For most of 2023 and 2024, the maritime decarbonization conversation followed a predictable script. LNG was the transition fuel — useful, but old. Methanol was the near-term answer — proven, deployable, increasingly green. Ammonia was the long-term answer — zero-carbon, scalable, the fuel of the 2030s and beyond. Hydrogen was the moonshot. Every panel agreed. Every consultancy report repeated it.

The orderbook through 2025 says something different.

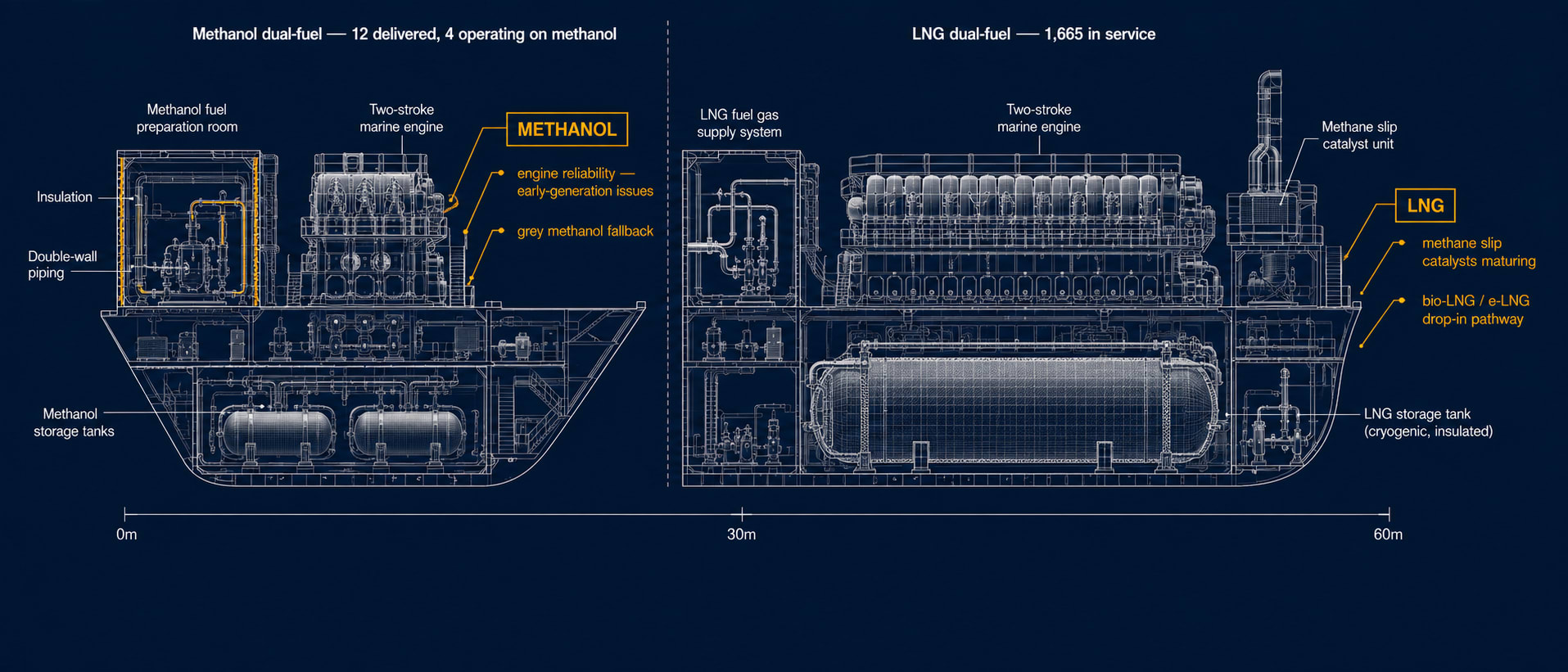

Methanol orders fell from 149 vessels in 2024 to 61 in 2025 — a sharp reversal after two years of exceptionally aggressive ordering. Ammonia recorded a total of five vessels ordered for the year. LNG, the “transition” fuel, took roughly 80% of all alternative-fuel new orders, up from 75% the year before. The overall alternative-fuel orderbook contracted 47% year over year, even as containership ordering held up. And Maersk — the carrier that built its decarbonization brand around methanol dual-fuel — is publicly working through engine reliability issues and operating much of its dual-fuel fleet on grey methanol because the green methanol supply chain has not yet caught up with the fleet.

This looks less like a temporary pause than a broad reassessment of deployment timelines.

What the 2025 Data Actually Shows

The data sources here are unusually clean for maritime markets. DNV's Alternative Fuels Insight platform, Clarksons Research, and Lloyd's Register all publish overlapping orderbook figures that converge on the same picture.

Headline figures for 2025 newbuild orders, drawing from DNV and Clarksons:

- Total alternative-fuel vessel orders: 275 (down from 581+ in 2024, a 47% decline)

- LNG-fuelled vessels: 188 orders, representing the dominant share of alternative-fuel tonnage

- Methanol: 61 orders (down from 149 in 2024)

- Ammonia: 5 orders for the full year

- Hydrogen: scattered orders, no meaningful fleet

- LPG and Ethane tanker orders: down 73% year over year

For context, the overall newbuild market also contracted, from 4,405 orders in 2024 to 2,403 in 2025. So part of this is industry-wide recalibration after an unusually heavy ordering cycle, with Chinese yard slot constraints, financing tightness, and post-2024 sentiment digestion all playing a role. But alternative-fuel orders fell more sharply than the broader market — meaning capital that did move in 2025 was disproportionately moving back to either LNG or conventional fuels, not into the next-generation fuels the industry has been promising.

Within the container segment, the picture is particularly striking. Of the 547 container vessels ordered in 2025, the fuel mix by tonnage was approximately 58% LNG, 36% conventional fuels, and 6% methanol. Three years ago, that split would have read as a methanol-led future. It now reads as a vote of confidence in LNG and an active hedge away from methanol.

Methanol's Specific Problem: The Maersk Lesson

If one company's experience defined the 2025 methanol pullback, it was Maersk's.

Maersk built its public decarbonization positioning around methanol dual-fuel. The company ordered 25 methanol dual-fuel containerships and, as of Q1 2026, operates a fleet of 21 dual-fuel methanol-capable vessels — making it by some distance the largest methanol-capable fleet in commercial operation. The Laura Maersk, the world's first large green methanol-enabled containership, has become a marketing fixture. The company signed a 500,000-tonne annual bio-methanol offtake deal with Chinese producer Goldwind, intended to fuel its first 12 dual-fuel ships from 2026 onward.

By mid-2025, the operating picture had diverged from the press releases.

Speaking at the Global Ocean Decarbonization 2025 seminar, Maersk's head of shipbuilding Ola Straby publicly acknowledged that only a small share of the company's delivered methanol-capable vessels were actually operating on methanol. The rest were burning conventional fuel. The reason, as reported across maritime trade press, was a combination of engine reliability issues — material selection problems, component reliability — and a green methanol supply chain that hadn't yet ramped to commercial scale.

“We are experiencing ongoing issues with our methanol dual-fuel propulsion engines,” Straby reportedly said. “As a result, we are burning grey methanol.”

“Grey methanol” in this context means fossil-derived methanol — methanol made from natural gas through conventional industrial processes, with carbon emissions in the same order of magnitude as conventional marine fuel. The long-term decarbonization case for methanol depends primarily on bio-methanol and e-methanol availability, not on grey methanol substitution. If a methanol-capable vessel is burning grey methanol, the climate advantage over conventional fuels narrows dramatically — especially on a lifecycle basis — and the operational complexity of the dual-fuel system is being absorbed for limited near-term gain.

Maersk's chief executive Vincent Clerc made the underlying issue explicit in a public statement in late 2024, asking the IMO to “close the price gap between green and fossil fuels.” Translated: green methanol is too expensive without policy intervention. Until that gap closes, the economics don't work.

Maersk is not abandoning methanol. The company continues to invest in dual-fuel tonnage, take delivery of new vessels through 2026 and 2027, and operate cargo-owner partnerships built around its ECO Delivery Ocean product. But the gap between strategic intent and operational reality has become harder to ignore — and the rest of the industry watched it widen in 2025.

Methanol the molecule is technically deployable. Methanol the supply chain is not yet at the scale the orderbook of 2023-2024 anticipated.

Ammonia: Five Ships Is Not a Breakthrough

The ammonia story is similar in structure but earlier in stage.

For three years, ammonia has been positioned as the long-term zero-carbon answer for deep-sea shipping. Engine manufacturers — WinGD, MAN Energy Solutions, Wärtsilä, J-Eng — have committed to delivering dual-fuel ammonia two-stroke engines from 2025 onward. Classification societies have rules. The IMO has issued interim guidelines. Pilot projects, including Fortescue's Green Pioneer and ammonia-fuelled tugs in Japan and China, have demonstrated technical feasibility.

The orderbook reality for 2025: five ammonia-capable vessels ordered for the full year, according to Clarksons.

The total operational ammonia-capable fleet at the end of 2025 was in the low single digits, mostly small demonstration vessels. The broader orderbook stood at roughly 39 ammonia-capable ships as of late 2025, with first commercial deliveries expected through 2026 and 2027. By any reasonable measure, this is the preparation phase of a transition, not the transition itself.

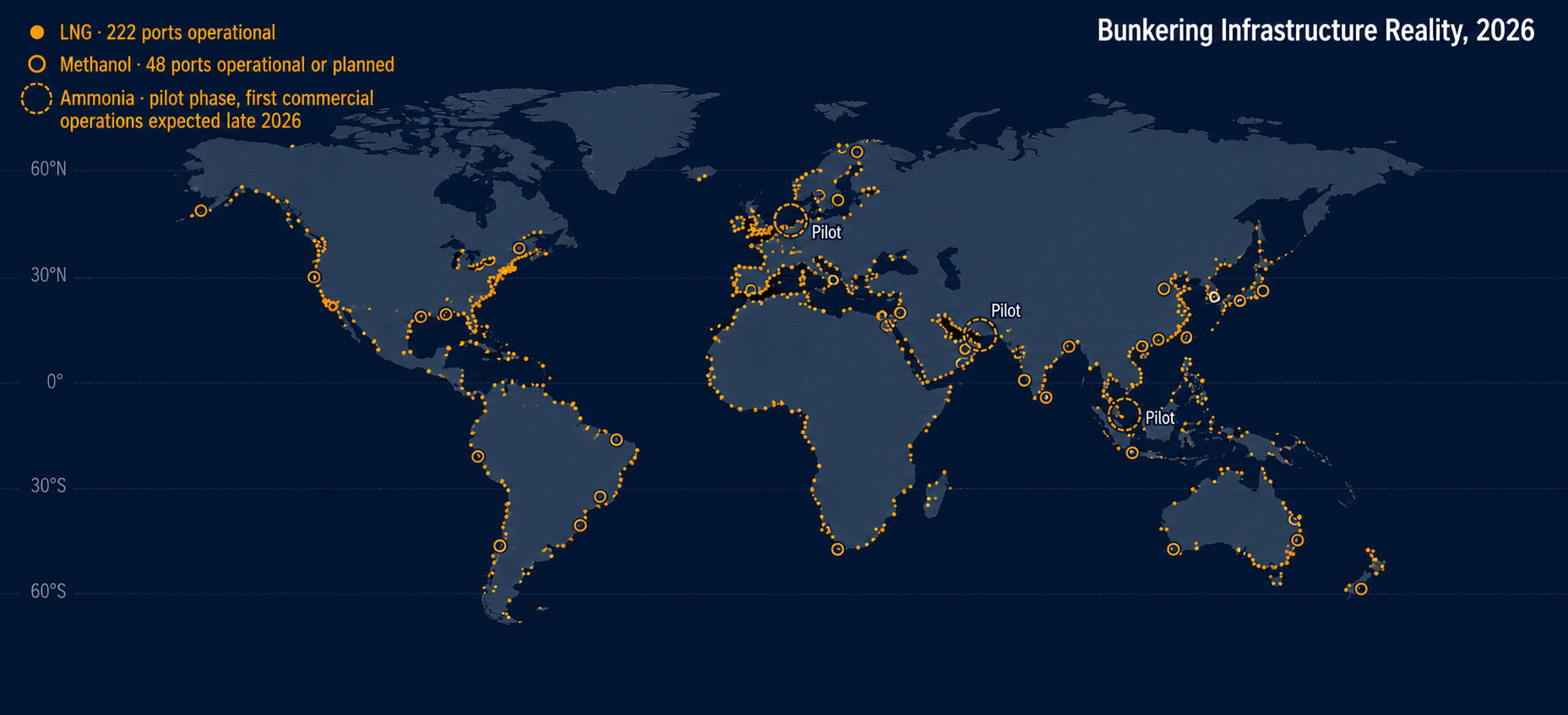

The barriers are operational, not philosophical. Ammonia is toxic at low concentrations — acceptable exposure limits are 20 to 50 parts per million, and concentrations above 2,000 ppm are fatal within thirty minutes. Crew safety frameworks are still being written. Bunkering infrastructure essentially doesn't exist — only a handful of ports are conducting safety studies, with Singapore targeting first commercial ammonia bunkering operations in late 2026. The IGF Code amendments that would provide binding global safety standards for ammonia-fuelled vessels are not expected before 2032.

Green ammonia, like green methanol, also has a price problem. Current estimates put green ammonia at two to four times the cost of conventional marine fuel, with no clear pathway to closing the gap without significant policy support.

The honest summary of ammonia in 2026: the engines are arriving. Small demonstration vessels are already operating. The regulations are catching up. The infrastructure still isn't. Five ships ordered in 2025 is roughly what that picture looks like.

Solid-State Batteries and Hydrogen: The Physics Problem

Two technologies that often appear in maritime decarbonization conversations belong in a different category: solid-state batteries and hydrogen propulsion.

For deep-sea shipping, the problem is still physics.

Battery-electric propulsion works extremely well in short-sea environments. Norway's electric and hybrid ferry network already proved that. The global marine battery system market was valued at roughly USD 1.66 billion in 2025 and is projected to roughly double by 2036. Hybrid architectures — where batteries assist diesel or LNG engines for load smoothing, peak shaving, and port operations — have reached commercial deployment in ferries, offshore support vessels, and some specialty segments.

Crossing the Pacific is a different problem. The energy density gap is fundamental: even the most advanced lithium-ion battery packs deliver roughly 1% to 2% of the volumetric energy density of marine gas oil. A VLCC running the Middle East to East Asia route consumes around 60 to 80 tonnes of fuel per day. Replacing that with batteries would require a vessel-sized energy storage system that no current technology supports.

Solid-state batteries are sometimes cited as the answer. The chemistry promises higher energy density, better safety, faster charging, and longer cycle life. The technology is real and is being commercialized in passenger vehicles. For maritime, however, solid-state batteries remain in pilot and early commercial phases. Deep-sea shipping does not struggle because the industry ignored batteries. It struggles because energy storage at ocean scale punishes any chemistry currently on the market.

Hydrogen sits in a similar position. The DNV orderbook shows four hydrogen-capable vessels currently on order, mostly in specialty segments — passenger vessels, small ferries, niche workboats. Hydrogen's volumetric energy density problem is even more severe than ammonia's, and the infrastructure for hydrogen bunkering is essentially nonexistent. Hydrogen will likely have a role somewhere in the eventual energy mix, but the role is not deep-sea commercial shipping in the next decade.

Battery hybrid systems are real, and for short-sea and specialty operations they are already commercial. Solid-state batteries and hydrogen, for ocean-going commercial shipping, are still future-tense.

Why Capital Moved Back Toward LNG

If alternative-fuel orderbook share for non-LNG fuels collapsed in 2025, LNG's share rose. By Clarksons' count, LNG accounted for roughly 80% of all alternative-fuel new orders in 2025, up from 75% in 2024.

The operational fleet tells the same story. As of March 2026, the global dual-fuel LNG fleet stood at 1,665 vessels in service, with another 982 on order — a near-term fleet of roughly 2,647 ships once the orderbook delivers. The container segment is leading: container lines have committed to LNG dual-fuel as their primary near-term decarbonization pathway, often paired with future bio-LNG and e-LNG drop-in compatibility.

Three factors explain the LNG return.

First, infrastructure. LNG bunkering is available at 222 ports globally. Methanol bunkering is available or planned at 48 ports. Ammonia bunkering is essentially zero. For a shipowner planning a 20-year capital asset, fuel availability is not a long-term concern to monitor — it is a near-term operational requirement that determines whether the vessel can trade profitably from day one.

Second, methane slip is becoming a managed problem rather than a structural disqualifier. Engine manufacturers have demonstrated significant reductions in methane slip from latest-generation Otto-cycle and high-pressure two-stroke LNG engines. Catalytic systems are reaching commercial readiness. The EU ETS treats methane emissions starting in 2026, which creates direct economic pressure to reduce slip — and that pressure is showing up in engine design and shipowner procurement specifications.

Third, the bio-LNG and e-LNG drop-in pathway means LNG dual-fuel ships have a credible path toward genuinely low-carbon operation as renewable methane supply scales. The same physical vessel that runs fossil LNG today can run bio-LNG or synthetic e-LNG in 2030 with no engine modification. That optionality has substantial financial value.

Put differently: LNG did not win the decarbonization argument on emissions intensity. It became the default hedge under uncertainty. Capital moved toward the option with the fewest immediate operational risks and the broadest future flexibility. That is a market behavior, not a climate verdict.

The 20% “Fuel-Ready” Buffer

One subtle but important piece of the 2025 data deserves attention. According to Clarksons, around 20% of vessel tonnage ordered in 2025 was classified as “alternative-fuel-ready” rather than committed to a specific alternative fuel.

This category did not exist as a meaningful share of the orderbook three years ago. Its emergence in 2025 is the most honest single signal in the data. Shipowners are explicitly buying optionality. They are not betting on a specific alternative-fuel future. They are buying ships that can move with the regulatory and infrastructure picture as it actually develops.

What 2026 Actually Looks Like

The IMO Net-Zero Framework, adopted at MEPC 84 in April 2025, introduces a carbon pricing mechanism that begins to take effect from 2028. The framework prices CO2-equivalent emissions on a tank-to-wake basis, with intensity reductions accelerating into the 2030s. In principle, this should close some of the price gap between green and fossil fuels and revive the methanol and ammonia orderbook.

In practice, three structural factors still need to resolve.

Green fuel production capacity has to scale. Goldwind's bio-methanol facility in China is one of perhaps a dozen projects worldwide expected to deliver commercial-scale green methanol in 2026 and 2027. Green ammonia production at industrial scale is even further behind. Until these supply chains exist, methanol and ammonia dual-fuel vessels cannot operate on the fuels they were built for.

Bunkering networks have to expand. Singapore's first ammonia bunkering target is late 2026. Methanol bunkering needs to grow from 48 ports to something closer to LNG's 222 to support a global trading fleet. This is a 5-to-10-year infrastructure buildout, not a 2026 deliverable.

Engine reliability has to improve. Maersk's methanol experience is not unique to Maersk. Early-generation dual-fuel engines for any new fuel will have material and reliability issues that take 2 to 5 years of fleet operation to identify and resolve. The methanol orderbook of 2023 to 2024 will be the data set that the industry learns from in 2026 to 2028.

The 2025 orderbook pullback is not a rejection of alternative fuels. It is a market signal that the deployment timeline shipowners considered credible in 2023 was wrong. The realistic horizon for meaningful non-LNG alternative-fuel fleet deployment has moved by several years — from “late 2020s” to closer to the early-to-mid 2030s.

That is the honest reset.

Implications

For shipowners: LNG-dual-fuel is the dominant near-term pathway. Methanol and ammonia remain credible long-term options but with delayed deployment. The “fuel-ready” optionality structure is increasingly the rational hedge for newbuilds in 2026 and 2027.

For cargo owners with internal emissions reduction commitments: 2025 confirmed that even leading carriers cannot fully execute on green fuel ambitions without functional supply chains. Cargo owner targets that depend on green methanol or green ammonia availability before 2030 will likely need revision.

For port and infrastructure investors: LNG bunkering remains the safest infrastructure bet through 2030. Methanol and ammonia infrastructure investments are still real but with longer payback timelines. The “early infrastructure leader” advantage that ports like Rotterdam and Singapore are positioning for is real, but the timing is later than originally projected.

For policymakers: the gap between regulatory ambition (IMO Net-Zero Framework, EU ETS coverage) and operational reality is still wide. Closing it requires either substantial carbon pricing — which the IMO framework begins to deliver from 2028 — or direct industrial policy support for green fuel production. Neither is currently sufficient to drive the 2030s transition that the 2050 net-zero target implies.

Shipping rarely rewards being technologically early. It rewards surviving long enough for the infrastructure to mature around you.

The industry has not abandoned alternative fuels. It has rescheduled them. The cost of that reschedule will show up in retrofit costs, stranded methanol orderbook risk, and a tighter 2030s transition window than the industry had planned for. Whether that window can still close is the open question.

The narrative didn't change. The capital did. Capital allocation tends to be less ideological than conference panels.