Bulk carrier size names sound technical from the outside, but they're really shorthand for trade patterns. A Capesize tells you the cargo is probably iron ore. A Panamax hints at grain or coal. A Supramax often means smaller ports and more flexible cargoes. Once you know what the labels mean, dry bulk headlines start reading less like jargon and more like a map of which trade is moving.

A single Capesize bulk carrier can haul around 180,000 tonnes of iron ore from Brazil to China in one voyage — enough steel-making material to support a mid-sized city for a year. Roughly 70% of the world's seaborne iron ore moves on this one ship class. That's why Capesize matters more than its fleet count would suggest.

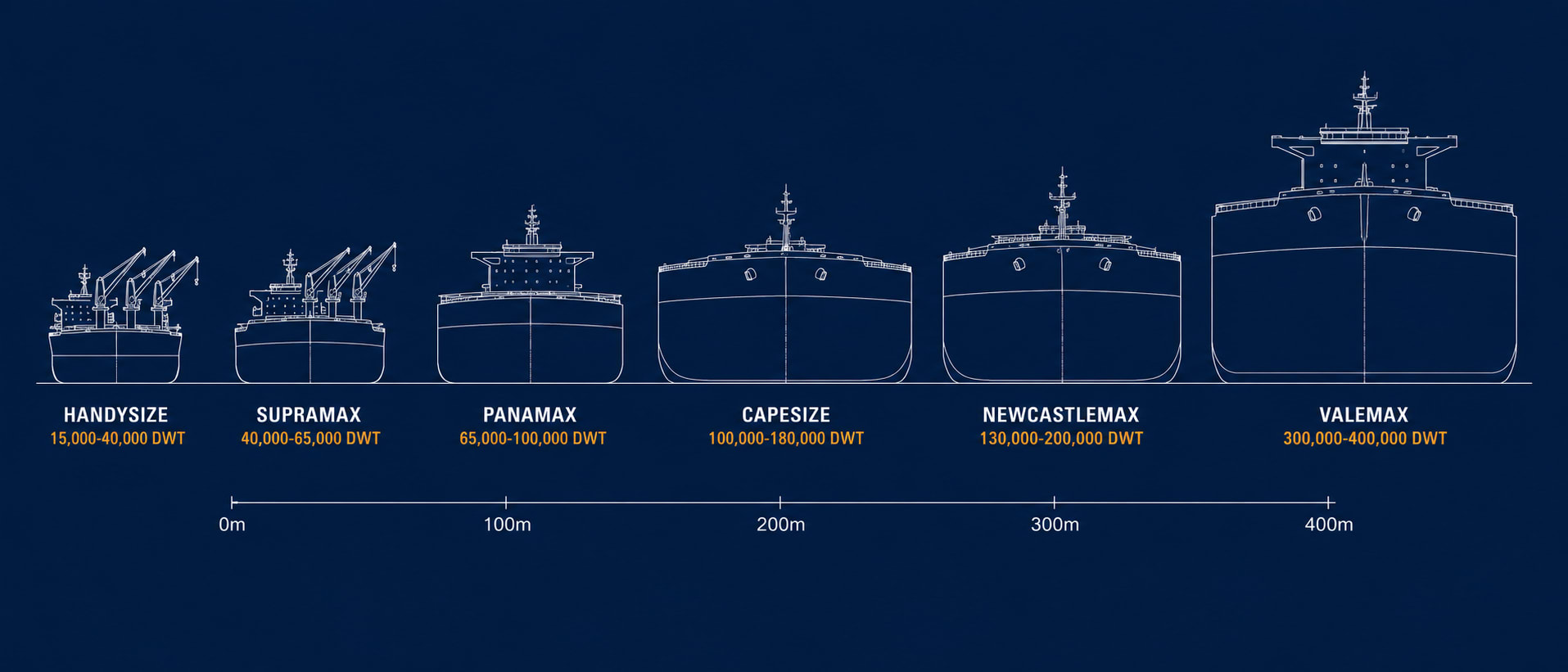

Let's walk through the classes, smallest to largest, and look at why each one exists. The names are not arbitrary. Most of them come from physical constraints: the depth of a canal, the width of a strait, the draft a particular port can handle. A few come from historical reasons that have stuck around.

The Smaller Classes: Mini, Handysize, Supramax

At the smaller end of bulk carriers, three classes do most of the work — and they do it where the bigger ships can't go.

Mini Bulk Carriers (3,000-15,000 DWT) operate as coastal and feeder vessels. They serve smaller ports without deep channels or large port infrastructure. Most have drafts under 8 meters and lengths under 130 meters. They carry the same cargoes the big ships move — grain, coal, ore, cement, fertilizer — just in smaller parcels to smaller terminals. Most never appear in industry market reports because their trade is regional and routine.

Handysize bulk carriers (15,000-40,000 DWT) are the workhorses of the minor bulk trades. About 150-200 meters long, with drafts of 10-12 meters. Almost all are geared — meaning they carry their own cargo cranes — which allows them to load and discharge at ports that lack shore-side cranes. That self-sufficiency makes Handysize ships the most flexible bulk carriers on the water. They serve smaller terminals, carry diverse cargoes (steel products, forest products, cement, minor ores), and operate on routes that wouldn't justify a larger ship.

Handymax (40,000-50,000 DWT) and Supramax (50,000-65,000 DWT) sit one step up. Most modern designs are actually Ultramax (60,000-65,000 DWT) — the latest iteration. They're still geared, still flexible, but with more cargo capacity. The BSI (Baltic Supramax Index) tracks freight rates for this class. Supramax has become the favored size for many tramp trades — the spot-market cargoes that don't fit dedicated routes — because the geared design lets them work almost any port without committing to a specific trade lane.

These smaller classes account for most bulk vessel movements but rarely make the news. When markets get exciting, the bigger ships do the moving.

Panamax and Kamsarmax

The first of the “headline” bulk classes is Panamax — typically 65,000-100,000 DWT.

The name comes from the original Panama Canal locks. A Panamax bulk carrier was designed to be the largest ship that could fit through those locks: beam under 32.31 meters, length under 294 meters, draft under 12 meters. The Panama Canal expansion in 2016 introduced larger locks (“Neopanamax” or “New Panamax”), but the original Panamax class name has stuck — partly because the dimensions still define what fits much of the world's older canal-adjacent infrastructure.

Panamax bulk carriers carry coal and grain on the biggest dry bulk trades. The classic Panamax routes are US Gulf grain exports to Asia, Australian coal to Japan, and South American grain to Europe. They are large enough to be economical on long voyages but small enough to access most major ports. The BPI (Baltic Panamax Index) tracks freight rates for this class — and the BPI is one of the four sub-indices that feed into the headline BDI.

Kamsarmax (around 82,000-85,000 DWT) is a sub-category of Panamax — named after the Guinean port of Kamsar, which has a maximum length restriction of 229 meters. Kamsarmax ships are slightly larger than the original Panamax design but still fit Kamsar, which made them attractive for the bauxite trade out of Guinea. The class name has since spread; many “Panamax” bulk orders are actually Kamsarmax. BIMCO's 2026 delivery forecast puts Panamax-class vessels (including Kamsarmax) at about 33.9% of all new bulker deliveries — the single largest class share.

If a port can take a Panamax, the trade goes Panamax. That's why this class continues to dominate the medium-haul bulk trades.

Capesize: The Headline Bulker

Capesize bulkers are 100,000-200,000 DWT. This is the class that shows up most often in dry bulk market headlines — because it's the workhorse of long-haul intercontinental dry bulk transport.

The name comes directly from the route limitation. Traditionally, Capesize vessels were considered too large to transit the Panama Canal — and often uneconomical or draft-restricted for the Suez Canal at full load. So on intercontinental voyages, they routed around either the Cape of Good Hope (southern Africa) or Cape Horn (southern South America). The “Cape” in Capesize refers to those two southern capes. The name reflects the routing reality the ships were built around.

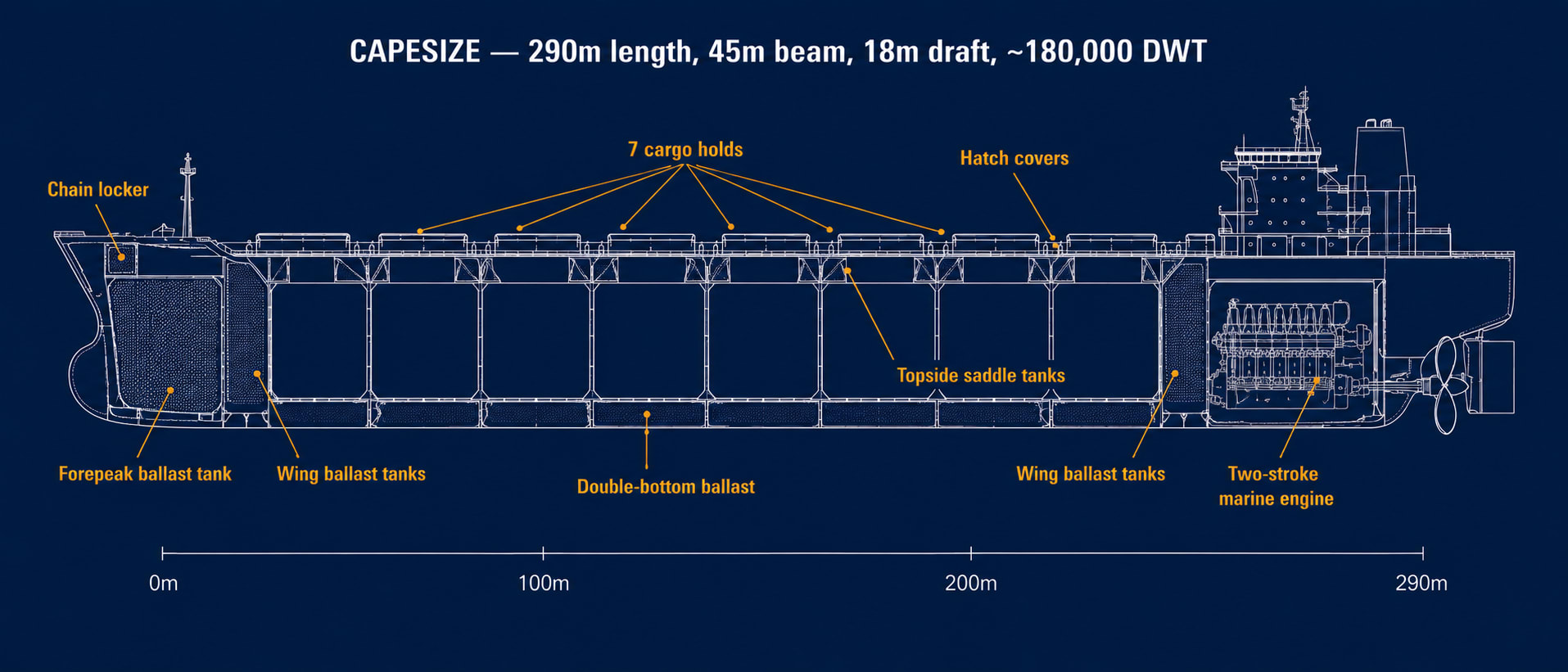

A typical Capesize is around 290 meters long, 45 meters wide, with a draft of 18 meters. It carries about 170,000-180,000 tonnes of cargo per voyage — primarily iron ore and coal. The benchmark Capesize freight reference is the Tubarão (Brazil) to Qingdao (China) route, often quoted as “C3.” In March 2026, the C3 rate stood at around $30/tonne. Brazil exported approximately 416 million tonnes of iron ore in 2025 — over half of it to China — and that single trade lane supports a large share of the global Capesize fleet.

About 70% of the world's seaborne iron ore moves on Capesize vessels, and iron ore accounts for roughly 63-65% of Capesize ton-mile demand. That linkage is one of the most important facts in dry bulk shipping. When Chinese steel demand moves, Capesize rates move first. The BCI (Baltic Capesize Index) is the most volatile of the BDI sub-indices, and it does most of the work behind BDI headline moves.

One operational detail worth knowing: bulk carriers, including Capesize and larger, almost never carry bow thrusters. Unlike container ships and many tankers, the dry bulk segment relies on tug assistance for berthing at the deep-water terminals where these ships operate. The marginal economics of dry bulk rarely justify the additional equipment, and the forepeak space that would house a thruster is more useful as ballast. When a Capesize arrives at port, the maneuvering is done by tugs, not by the ship itself.

The other operational constraint: Capesize ships need deep water at both ends. They can only call at deep-water ore and coal terminals — Tubarão, Saldanha Bay, Port Hedland, Dampier, Qingdao, Rizhao. That's not many ports. Roughly 80% of Capesize voyages move between just a handful of loading and discharge terminals.

Newcastlemax, VLOC, Valemax: The Largest

Above the standard Capesize range, three sub-classes carry specific dedicated trades.

Newcastlemax (around 185,000 DWT) is named for the Australian coal port of Newcastle — the world's largest coal export terminal. A Newcastlemax is the largest vessel that fits Newcastle's loading constraints: roughly 300 meters length, 50 meters beam. It exists almost entirely to load Australian coal for Asia. Like Kamsarmax, it's a port-specific dimensional limit that became a vessel class.

VLOC — Very Large Ore Carrier — refers to bulk carriers of 200,000-400,000 DWT. These are dedicated iron ore carriers, almost entirely deployed on a single trade: Brazil to China. The distance is over 20,000 kilometers — long enough that scale economics dominate. A VLOC moves twice the cargo of a standard Capesize on the same voyage. The largest sub-class, Valemax (built starting in 2008 for Brazilian miner Vale), reaches around 400,000 DWT — large enough that the first Valemax cargoes faced restrictions at Chinese ports, prompting Vale to build dedicated transshipment hubs in Malaysia and the Philippines.

The trade-off across all these very large bulkers is the same as with VLCCs in tanker shipping: extraordinary economics on the specific trade they were designed for, almost no flexibility for anything else. A Newcastlemax built for Newcastle coal can't economically shift to grain. A Valemax built for Brazil-China iron ore can't easily redeploy to West Africa. Most of them spend their working lives doing essentially the same voyage over and over again.

Why Dry Bulk Markets Move So Hard

There's one feature of dry bulk markets worth understanding because it explains a lot of headline volatility: ship supply reacts slowly.

Bulk carriers take roughly two to three years to build from order to delivery. A surge in iron ore demand can move freight rates immediately, but the fleet response — new ships actually entering service — takes years. When demand falls, ships can't easily exit either; demolition is slow and cyclical, and most owners would rather lay up a vessel than scrap it. That mismatch between fast demand and slow supply is one reason the BDI can move 20-30% in a week and 70-80% across a quarter. Dry bulk markets don't glide. They lurch.

Distance amplifies it. In dry bulk shipping, ton-mile demand matters almost as much as cargo volume. A Capesize tied up on a longer Brazil-China voyage stays unavailable for longer than the same ship on a shorter Australia-China voyage. That “effective supply” effect is one reason Brazilian iron ore flows tend to move freight rates more sharply than Australian flows, even when the volume changes are similar.

Why the Names Persist

There's a small irony in bulk carrier class names: many of them are named after constraints that have changed.

Panamax ships are named for canal locks that were superseded in 2016. Kamsarmax ships are named for a Guinean bauxite port. Newcastlemax ships are named for an Australian coal port. Capesize ships are named for two southern capes that most of them now routinely sail around — not as a constraint, but as the standard route.

The names persist because brokers and chartering desks still use them as shorthand for a particular operational profile — how much cargo it carries, where it can go, what it usually does. Everyone in the industry immediately understands the cargo profile and port access limits attached to each name. Renaming would mean relearning a set of associations that already work. So the names stay, even as the underlying constraints shift.

Reading the News With This in Mind

When a news article mentions a specific bulk carrier class, the class is doing work in the sentence — telling you something about the cargo, the route, and often what kind of story is being told.

A headline about Capesize rates is almost always about iron ore or coal on Brazil-China, Australia-China, or South Africa-Asia. A story about Panamax fixtures usually involves grain or coal on medium-haul routes. A Supramax move points to minor bulk or geared-vessel work in less-developed ports — Indian Ocean, Southeast Asia, Latin America, West Africa. Handysize headlines are rare; when they appear, the story is usually about niche regional cargo.

When the same story uses the generic phrase “dry bulk freight rates,” check the context. If the figure quoted is in millions of tonnes per day or quotes a Brazil-China or Australia-China route, you're looking at Capesize. If the cargo mentioned is grain to Asia, it's probably Panamax. If the ship has cranes mentioned, it's almost certainly Supramax or Handysize. The BDI itself is a composite of four sub-indices — Capesize, Panamax, Supramax, Handysize — and Capesize has the heaviest influence on BDI moves.

The 30-Second Version

- Bulk carriers are sorted by deadweight tonnage (DWT) into named size classes.

- Mini (under 15k), Handysize (15-40k), Supramax/Ultramax (40-65k), Panamax (65-100k), Capesize (100-200k), VLOC/Valemax (200-400k).

- Most size names encode a physical constraint: Panamax (canal locks), Kamsarmax (Guinean port), Newcastlemax (Australian coal port), Capesize (two southern capes).

- Capesize is the headline bulker — about 70% of the world's seaborne iron ore moves on this one ship class.

- Iron ore (Brazil and Australia to China) drives most Capesize freight rates and accounts for the bulk of BDI movement.

- Dry bulk markets are volatile because fleet supply takes years to respond to demand swings.

Closing

Bulk carrier size classes are one of those bits of industry shorthand that look forbidding from the outside and turn out to be straightforward once you see the logic. They encode physical constraints — canal locks, port depths, route economics — and they organize a fleet of thousands of ships into a handful of operational categories.

Most maritime headlines about dry bulk mention a class by name, and the class is doing work. Knowing whether you're reading about a Capesize or a Supramax tells you which trade lane is moving, which freight index is responding, and roughly what cargo is at stake.

The next time you see “BDI surges 20%” or “Brazil-China iron ore rates” in a headline, you'll know which trade is doing the work.