In early 2026, Ukraine's intelligence services published a catalog of 1,337 vessels they classify as the shadow fleet. Windward, using different criteria, classifies over 1,000 tankers as gray or dark. The IMO, in its April 2026 GISIS update, flags 367 tankers as sailing under false registrations. Lloyd's List Intelligence counts 1,423 tankers involved in sanctioned oil trading — 921 of which are under active US, EU, or UK sanctions.

Four methodologies. Four different numbers. The same structural conclusion.

The numbers differ because the definitions differ. Ukraine counts vessels suspected of involvement in Russian oil export. Windward counts behavioral markers — AIS manipulation, flag changes, opaque ownership. The IMO counts vessels whose registration documents contain demonstrably false information. Lloyd's List counts vessels that have physically carried sanctioned barrels.

The precise count is less important than the capacity it represents. S&P Global Market Intelligence identifies 978 oil tankers above 27,000 DWT operating outside established norms, with combined capacity of 127 million deadweight tonnes — approximately 18.5% of global tanker market capacity. The conclusion is consistent regardless of which methodology you trust: roughly one in five oil tankers now operates outside the system that prices freight visibly.

The shadow fleet is not a competitor. It is a subsidy. Its function is to absorb the costs — insurance, legal exposure, reputational risk — that mainstream operators will not carry, so that sanctioned crude can reach buyers at prices that would be impossible if those costs had to be paid at market rates. The freight market consequence of that function is not competition with the mainstream fleet. It is permanent supply removal from it.

The three-tier market

The shipping market has never been monolithic. Flag registries, ownership structures, and insurance arrangements have always varied. What changed after 2022 is that the variation became structural: vessels sorted themselves into tiers based on what kind of cargo they would carry, under what terms, for what counterparties.

The Windward classification is the most analytically useful because it distinguishes between vessels that are excluded and vessels that are friction-loaded. A vessel using a flag of convenience with opaque ownership is not the same as a vessel running dark AIS in the Gulf of Oman with a single-vessel shell company and a false cargo origin. The first may be compliant. The second is not. The gray zone between them is where the market impact is concentrated.

The gray tier is commercially significant because it is large. Vessels with one flag change in twelve months, a single-layer corporate structure, and occasional AIS gaps are not sanctioned. They are not on any list. But oil majors will not charter them, IG P&I clubs will not insure them at standard terms, and port state control authorities will inspect them more frequently. The gray tier is not outside the mainstream market — it is priced out of it by friction.

The consequence is functional supply removal without any formal designation. A vessel that was chartered freely in 2021 may now require weeks of compliance review before a major oil company will use it. In a market where freight windows are measured in days, weeks of compliance review is supply removal in practice.

How it works

The shadow fleet operates through four coordinated evasion mechanisms. Each addresses one dimension of the enforcement system. Together, they create a parallel supply chain that is resistant to disruption at any single point.

The AIS manipulation is the most visible mechanism. In the months following the February 2022 sanctions package, Windward recorded over 200 AIS manipulation incidents per month in areas associated with Russian crude loading. A vessel that went dark for twelve hours in the Kerch Strait and reappeared off the coast of Turkey with a full cargo manifest had, legally, a break in its documented history. That break is the gap through which cargo origin is laundered.

Ship-to-ship transfers address the second layer. If AIS can be used to hide where a ship was, STS can hide what it is carrying. Crude pumped from a sanctioned VLCC to a non-sanctioned Suezmax in the Gulf of Oman arrives at a Chinese refinery with a fresh cargo history and a clean bill of lading. The physical oil has not changed. The paper trail has been reset. The STS transfer hotspots — the Gulf of Oman, the waters near Ceuta, the Straits of Malacca south of Malaysia — are not random. They are jurisdictional gaps where enforcement is light and transfer conditions are favorable.

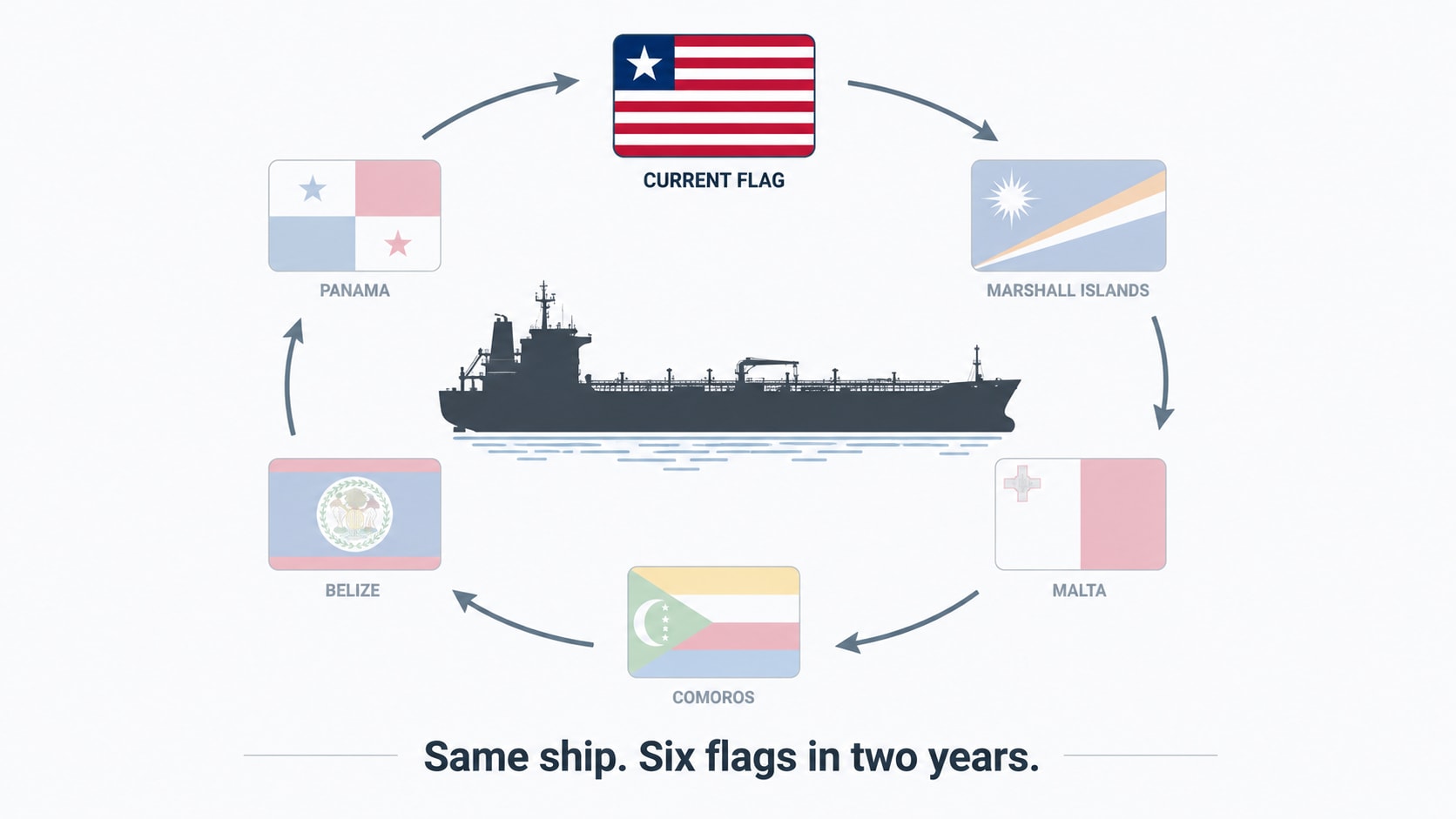

Flag changes address the third layer. When a flag state is pressured to withdraw registration from shadow fleet vessels — as Palau, Tuvalu, and Belize have all done under US pressure — vessels simply re-register elsewhere. Gabon, Cameroon, and São Tomé and Príncipe have all seen sharp increases in tanker registrations since 2022. The IMO's April 2026 count of 367 false-flagged tankers represents only the cases where registration documents contain demonstrably incorrect information. The actual number of vessels using compliant-but-accommodating flag registries is substantially higher.

The shell company structure is the foundation that makes the other three mechanisms durable. A single-vessel company registered in a jurisdiction with no public beneficial ownership registry can be abandoned after sanctions designation, replaced with a new entity, and the vessel transferred within days. OFAC's designation list grows. The fleet adapts. The ship keeps trading.

The numbers

The definitional dispute between Ukraine, Windward, the IMO, and Lloyd's List is sometimes treated as a reason to discount the shadow fleet's significance. It is not. The different counts reflect different measurement choices, not different realities. The vessel that Ukraine counts as a shadow fleet member because it loaded at Ust-Luga in January 2026 — the same vessel that Windward classifies as dark because it has changed flag three times and run dark AIS twice in six months — is the same ship the IMO flags for using a false Comorian registration. The databases overlap imperfectly. The fleet they are counting is the same fleet.

Ukraine's intelligence catalog, published in February 2026, lists 1,337 vessels. Windward's real-time platform classifies over 1,000 tankers as gray or dark on any given day. The IMO's GISIS database records 367 tankers operating under false registrations as of April 2026.

The capacity dimension is more telling than the vessel count. S&P Global Market Intelligence identifies 978 oil tankers above 27,000 DWT operating outside established norms, with combined capacity of 127 million deadweight tonnes — approximately 18.5% of global tanker market capacity. Lloyd's List Intelligence places the total number of tankers involved in sanctioned oil trading at 1,423, of which 921 are subject to active US, EU, or UK sanctions. Four different methodologies. Four different numbers. The same structural conclusion: roughly one in five oil tankers worldwide now operates outside the system that prices freight visibly.

The capacity figure matters more than the vessel count. A 127 million DWT capacity block operating outside the mainstream system represents a structural removal from the freight market that cannot be offset by adding vessels at the margin.

The supply removal math

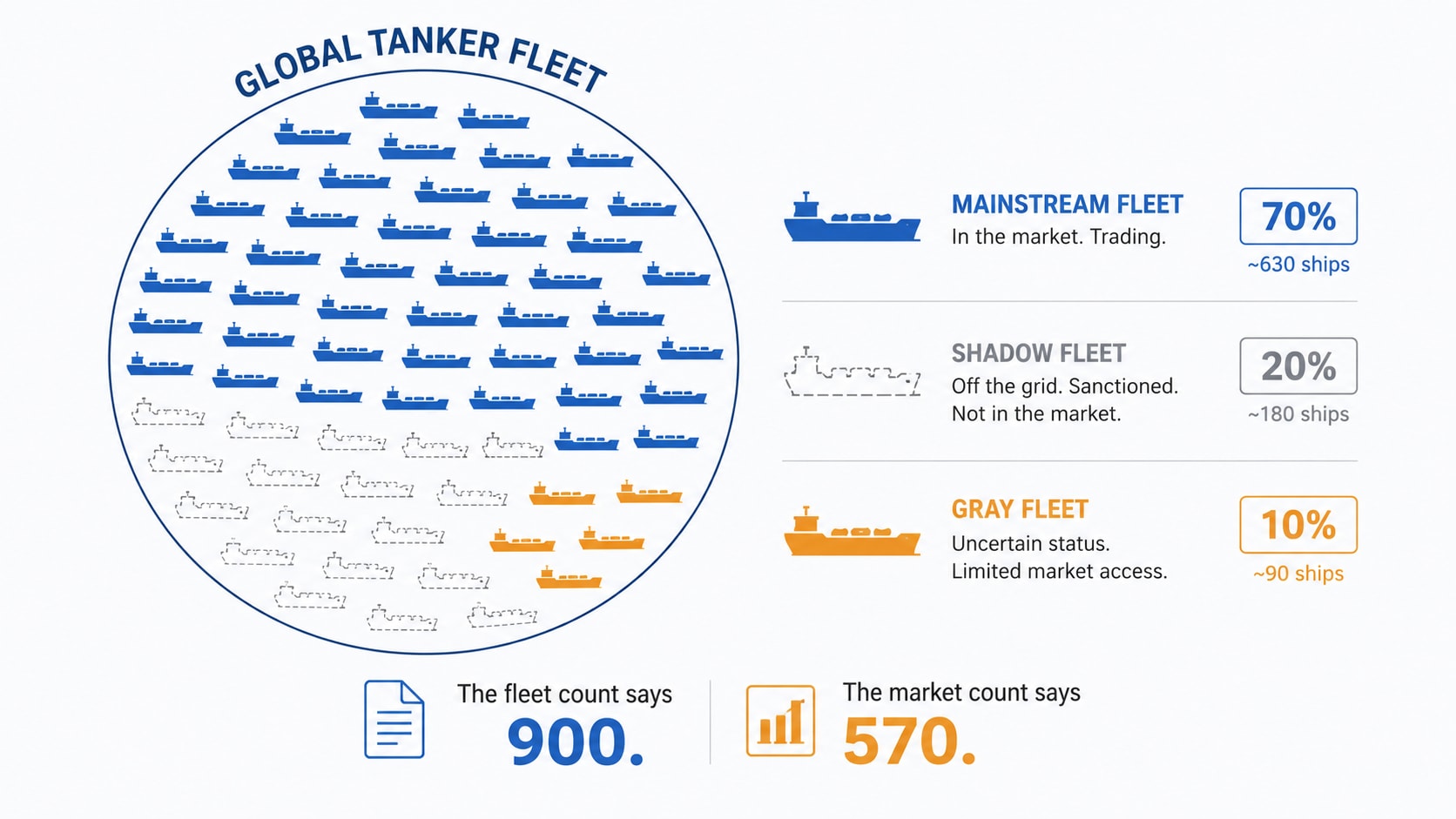

The arithmetic that connects the shadow fleet to the freight rate floor is straightforward. The global VLCC fleet numbers approximately 900 vessels. Tankers International and other pool operators estimate that roughly 200 VLCCs are either formally sanctioned or have carried sanctioned barrels sufficiently recently to be excluded from mainstream oil major vetting. That leaves approximately 700 commercially available VLCCs.

Of those 700, approximately 130 are older than 20 years. These vessels face escalating survey costs, declining charterer acceptance under CII/EEXI frameworks, and hull design specifications that predate IMO 2020. They may still trade — but they are increasingly excluded from oil major approved vessel lists and from the fixtures that set the visible rate. Effective mainstream supply is closer to 570.

Against that 570-vessel effective fleet, annual demand growth of 2–3% per year — driven by long-haul crude flows from West Africa and South America to Asia, Chinese strategic petroleum reserve additions, and the extended voyage distances created by Hormuz diversions — creates a structural tightening that no near-term delivery wave resolves. The ships ordered in 2025 and 2026 arrive in 2028 and 2029. The gap between now and then is unfilled.

The shadow fleet's market consequence is not that it competes with the mainstream fleet for the same cargoes. It does not. It carries crude that mainstream operators will not carry, to buyers that mainstream operators cannot serve, under terms that mainstream operators cannot accept. It does not take business from the mainstream fleet. It removes itself from the pool the mainstream fleet draws from.

The 200 VLCCs in the shadow fleet are not available for mainstream charter. They will not become available through better enforcement alone — their operational model, ownership structure, and flag registration are optimised for the parallel market. The 130 ageing VLCCs are not available because their commercial fitness is declining regardless of sanctions. The 570 that remain are the supply the market works with. This is the structural floor.

The enforcement wave

The enforcement environment changed materially in the first half of 2026. What had been a pattern of financial sanctions and administrative designations shifted toward physical interdiction. Warships, commandos, and seizure orders replaced sanctions lists as the primary enforcement tool.

Spain's Operation Marinera, conducted in coordination with NATO maritime surveillance, identified a series of shadow fleet vessels transiting Iberian waters and generated the intelligence dossiers that enabled subsequent seizures. The operation demonstrated that coordinated maritime surveillance could produce actionable enforcement cases — but the seizures required a legal theory that could survive challenge under international law.

The legal doctrine underpinning these seizures is straightforward: a false flag forfeits the right of innocent passage under UNCLOS. France established the precedent on January 22 when commandos from a Horizon-class frigate, transported by two NH90 helicopters, boarded the Grinch — a UK-sanctioned, Comorian-flagged tanker — in the Alboran Sea. The Tagor seizure on June 1 extended that doctrine 740 km into the Atlantic. The UK's Smyrtos operation on June 14 reinforced it in the Channel. The legal basis is now tested and repeating: prove the flag is false, and the vessel loses its sovereign protection.

Belgium, France, and the UK have each moved to detain vessels carrying documentation inconsistent with their registered flag states. The pattern is consistent: a vessel claiming Comorian, Gabonese, or Panamanian registration with crew documents, cargo papers, or AIS records that cannot be reconciled with that registration faces seizure in European waters. In each case, the flag state cooperated by confirming the registration was falsified or invalid.

The Bella I incident in the Baltic extended the pattern to Russian escort operations. When the Bella I — a shadow fleet crude carrier tracked by Estonian maritime authorities — was approached by a NATO patrol vessel, Russia dispatched a submarine to the area. The deployment, confirmed by the Wall Street Journal, CBS News, CSIS, and The War Zone, represented the first direct use of Russian naval assets to protect a commercial shadow fleet operation. Russia regards the shadow fleet as a strategic asset worth defending with military force.

Sea Owl I, detained in Danish waters in May, followed the same pattern as Grinch — Comorian flag, UK sanctions designation, crew records inconsistent with the vessel's documented history. The Danish detention produced the most complete cargo chain-of-custody documentation of any shadow fleet seizure to date: a loading terminal in Russia, four STS transfers across three jurisdictions, a final destination at a Chinese refinery.

The enforcement acceleration has three limits. First, it applies only in waters where enforcement states have jurisdiction — European seas, NATO surveillance zones, and cooperating flag states. The Gulf of Oman STS zone, the waters north of Malaysia, and the East China Sea are outside this perimeter. Second, the seizure rate remains a fraction of the designation rate. Hundreds of vessels have been sanctioned; dozens have been physically detained. The fleet absorbs the attrition. Third, Russian state protection of shadow fleet operations — including submarine deployment — raises the cost of interdiction in contested waters.

The growth trajectory

The shadow fleet has grown continuously since 2022. It has not yet peaked.

The EU's sanctions program covers approximately 600 vessels — roughly two-thirds of the vessels identified as part of Russia's shadow fleet infrastructure. OFAC's designation coverage is approximately 40% of the estimated total. No enforcement program has yet produced a year-on-year net reduction in shadow fleet size. The addition rate — new vessels entering through purchase, flag change, and corporate restructuring — exceeds the removal rate through seizure, sanctions compliance, and designation.

The growth trajectory has two drivers. The first is the economic incentive: shadow fleet operators earn a premium for carrying sanctioned crude that compensates for higher operational costs, insurance limitations, and legal risk. As long as that premium persists — and it has shown no sign of compressing materially — the economic logic of shadow fleet operation is sound.

The second driver is the political geography of crude supply. Russian, Iranian, and Venezuelan crude must reach markets. The producers have no incentive to reduce output, and the buyers — primarily Chinese, Indian, and some Southeast Asian refiners — have strong economic incentives to access discounted crude. The shadow fleet is the mechanism by which discounted sanctioned crude reaches willing buyers. It is not a temporary arbitrage. It is an institution.

The consequence for the mainstream freight market is the structural floor that the shadow fleet's supply removal creates. The Hormuz reopening analysis distinguished between the risk premium layer of VLCC rates and the structural floor layer. The risk premium compresses when the Strait opens. The structural floor — set by the 570-vessel effective mainstream supply against 2–3% demand growth — does not compress because it is not a risk premium. It is a supply condition. The shadow fleet is the primary mechanism by which that condition is maintained.

For TCE calculations, the shadow fleet's effect is not captured in voyage cost inputs — bunker, port dues, canal fees — but in the freight rate denominator. A rate floor that is structurally higher than the 2018–2021 average, because the effective supply pool is structurally smaller, produces a higher TCE on every voyage even when spot rates are not at historic peaks.

The P&I Club system is the clearest structural divide between the mainstream and shadow fleets. The International Group's mutual reinsurance pool is unavailable to vessels operating outside its membership criteria — criteria shadow fleet operators cannot meet while maintaining their evasion structures. The war risk insurance cost differential represents not merely a premium gap, but different insurers, different policy structures, and in some cases no insurance at all — risk carried directly by the operating entity or by state-backed Russian guarantee structures.

The flags of convenience that enable the shadow fleet's operational model are the same registries that the labour abandonment data identifies as concentrated sources of seafarer abandonment cases. The structural enablers of the shadow fleet — thin-capitalised operators, opaque corporate structures, flag registries that do not enforce crew payment — are the same enablers that produce the highest rates of crew abandonment in the broader maritime system.

The fleet count says one thing. The effective supply says another. The shadow fleet did not create that gap by competing with the mainstream market. It created it by leaving. That is the subsidy — absorbed quietly, priced into every mainstream voyage that follows.