Every commercial ship of any real size — bulker, tanker, containership, LNG carrier — comes out of the water at least once every five years. It has to. The rules that govern the sea require it, and the classification societies that certify each hull enforce it.

In 2026, according to Clarksons Research, more than 12,000 vessels are scheduled for what the industry calls a special survey — the full inspection that a ship undergoes every five years to keep its class certificate valid. The figure comes from Clarksons' fleet-age modelling, which forecasts survey volume from class-society registries several years in advance. That certificate is what keeps a ship insured, insurable, and legally free to trade. Lose it, and the vessel stops earning money.

Which raises a simple question that doesn't get asked very often: where do all those ships go?

The short answer is roughly 723 yards spread across 95 countries. The longer answer is that the traffic is very unevenly distributed — and increasingly, three or four places do most of the work.

The calendar that drives everything

The rule that structures the ship repair industry is not economic; it's regulatory.

Under SOLAS — the International Convention for the Safety of Life at Sea, administered by the International Maritime Organization — cargo ships above 500 gross tons and all passenger ships on international voyages must undergo periodic surveys. The two that matter most for repair yards are the intermediate survey, performed roughly 2.5 years into a five-year certificate cycle, and the special survey, which comes at the end of that cycle.

The intermediate survey doesn't always require a ship to be lifted out of the water. Under certain conditions, an underwater inspection by divers, filmed and reviewed by a class surveyor, is accepted in place of a dry-docking. This is called an in-water survey, and it's common on tankers and bulkers with clean recent histories.

The special survey is different. This one almost always requires the hull to come out. Everything a diver cannot fully verify — the state of the bulbous bow, the propeller shaft seals, the underwater fittings, the coating condition beneath the waterline — gets a close look by a surveyor standing next to the ship on dry ground.

Because the survey cycle is set at five years from the day the certificate was issued, and because the world fleet is very large and very old, the flow of ships into repair yards is close to constant. In practice, yards forecast their workload years in advance from the class registry alone.

What actually happens during a dry-docking

The picture people have in mind — a giant ship sitting on blocks while workers paint it — is not wrong. Painting is a big part of it. But it is not close to the full list.

A typical special-survey dry-docking — whether the ship is 5, 15, or 25 years old — tends to include the same sequence of work:

- Hull cleaning. The underwater portion of the hull accumulates a rough layer of marine growth — barnacles, algae, and biofilm — that increases drag by several percent and burns extra fuel every hour of the ship's life. Removal is done by high-pressure water jets and mechanical scrapers.

- Anti-fouling paint. After cleaning, the hull is re-coated with a specialized paint that either slowly releases biocides or presents a low-friction surface that discourages growth. This one job can account for 15–25% of the total dry-dock invoice.

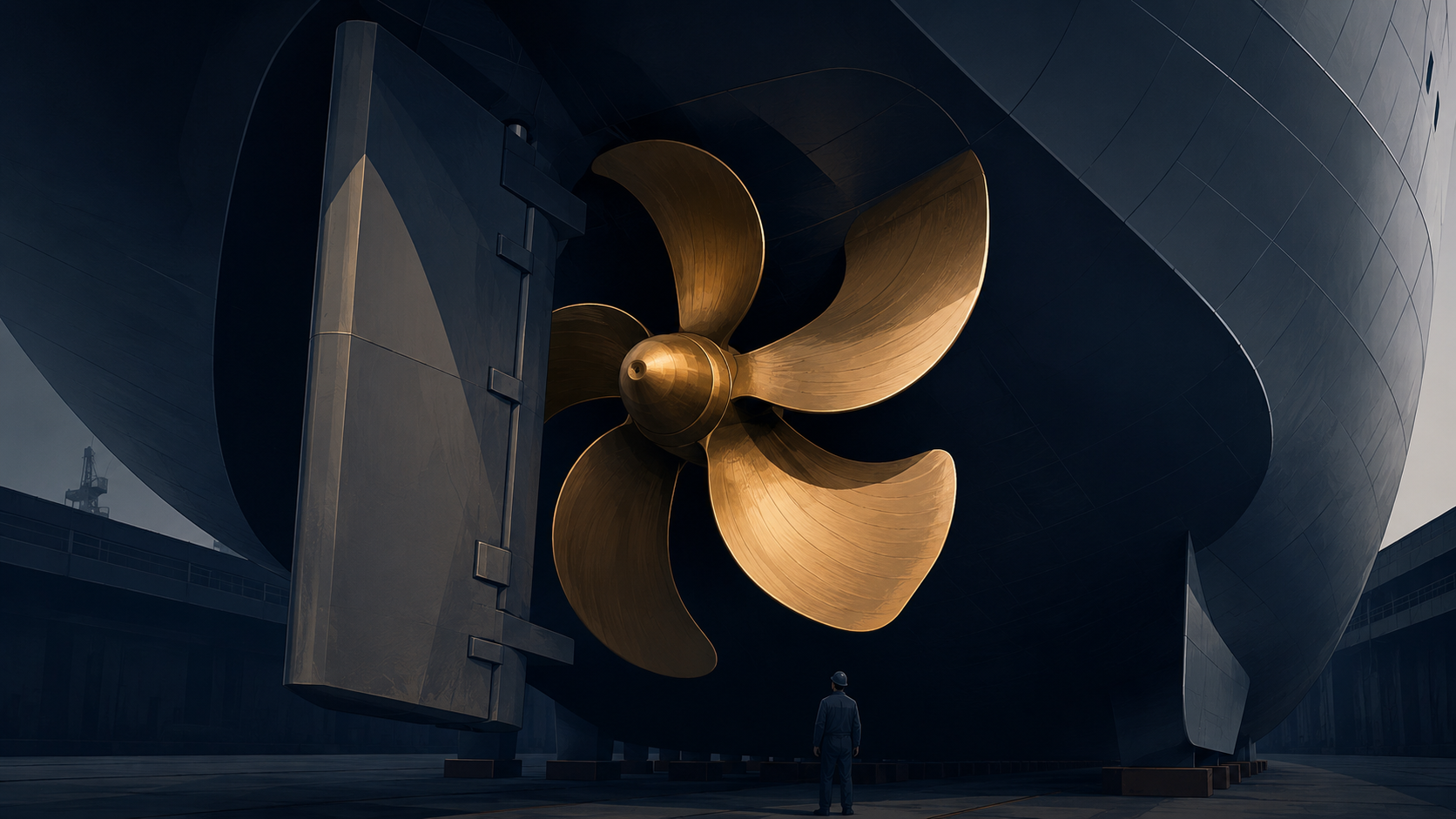

- Propeller inspection and polishing. The propeller is arguably the single most performance-sensitive part of the hull. Small nicks and roughness translate directly into fuel consumption. Polishing recovers efficiency; damage requires balancing or blade replacement.

- Rudder inspection. Steering-gear alignment, rudder stock bearings, and seal integrity are all checked while the ship is stationary and accessible.

- Sacrificial anodes. The zinc or aluminum anodes bolted to the hull below the waterline prevent electrolytic corrosion of the steel. They are consumed over the five-year cycle and replaced during dry-docking.

- Sea chests and underwater valves. The intakes and discharges that pass through the hull — sea chests for cooling water, overboard discharges for ballast and bilge systems — get inspected and refurbished. These are the only valves that a dry-docking really needs to open up, because they can't be reached from inside the ship in a floating condition.

- Steel renewals. Where the hull has thinned from corrosion or wear beyond class limits, plates are cut out and welded in. This is expensive, and the amount required scales up sharply with vessel age.

- Underwater survey work. The class surveyor uses this window to verify the ship's official condition and update its records.

Main-engine work usually happens in parallel, but it is not dry-dock-dependent. Piston overhauls, cylinder liner replacements, and fuel system servicing can be performed at pier-side just as easily. Owners often schedule a heavy main-engine overhaul to coincide with the yard visit for scheduling convenience, but if the engine work runs long, the ship can be re-floated and finish the engine job alongside.

The total time in dock, for a well-run bulker, is typically 10 to 18 days. For a containership or LNG carrier with retrofit work bolted on, it can stretch to 30 or more.

The geography

At a global level, the repair industry is a roughly $40 billion business, and demand grows by around 3% per year — driven not by new ships (those are handled by builders), but by the fact that the fleet keeps getting bigger and older. The size figure is a market-research aggregate (Business Research Insights and comparable industry reports); the 3% growth reference traces to Clarksons commentary quoted by Riviera Maritime Media and other trade press.

Asia-Pacific handles the largest share. Estimates from market researchers put the region at around 41% of global repair revenue. Within Asia, three countries — China, Singapore, and South Korea — together account for roughly half of all dry-dockings performed worldwide. Their roles are not the same.

China dominates on volume. The country's coastline hosts more than 500 licensed shipyards, and its major players — COSCO Shipping Heavy Industry and China Shipbuilding Industry Corporation — run yards in Shanghai, Guangzhou, Tianjin, and Dalian that between them process several thousand vessels per year. Chinese yards work across every segment, from Handysize bulkers to VLCCs, and their competitive edge is scale plus turnaround speed.

Singapore is the specialist. The country's 42 registered ship-repair yards, concentrated in Tuas and on Jurong Island, focus on tankers, offshore support vessels, and increasingly on retrofit work for dual-fuel and LNG conversions. Seatrium — formed in 2023 through the merger of Sembcorp Marine and Keppel Offshore & Marine — anchors the market. Its Tuas Boulevard Yard is one of the largest single-site repair complexes anywhere.

South Korea plays a different role. The country is the world's second-largest shipbuilder by CGT — behind China, which has dominated total tonnage output since the late 2010s — and its yards lead in specific high-value segments such as LNG carriers, large containerships, and dual-fuel newbuilds. In pure ship repair, though, Korean yards concentrate on high-value refit work: LNG carrier conversions, methanol dual-fuel retrofits, and offshore projects. Straight dry-dockings for bulkers and mid-sized tankers flow increasingly toward China and Southeast Asia.

The Middle East's largest repair capacity historically sat at Drydocks World Dubai, owned by DP World. The complex — with three graving docks and a large surrounding yard area built out through the 2000s and 2010s — remains a major regional facility specializing in ultra-large crude carriers, offshore floating production unit conversions, and vessels serving Middle Eastern trades. Its volume has moderated from its peak years as competing yards in India (Cochin Shipyard) and elsewhere in the region have expanded, but it retains an anchor role for VLCC and FPSO work in the Gulf.

Europe holds around 26% of the global market, but its work is fragmented across national specialties. Norwegian and Dutch yards handle offshore support vessels and short-sea tonnage; Italian yards, led by Fincantieri, do most of the cruise sector's dry-docking; Turkish yards in Tuzla have become the mid-market default for European bulkers looking for shorter lead times than Northern Europe can offer.

The United States is defined almost entirely by defense. Naval maintenance contracts to Huntington Ingalls Industries, General Dynamics NASSCO, and BAE Systems account for most of the domestic ship-repair economy. Commercial dry-docking exists but is limited by the Jones Act to U.S.-flag operators; the international commercial fleet almost never calls at U.S. yards for scheduled work.

Why 2026 is busy

Three forces have pushed dry-dock demand well above trend.

The first is age. According to Clarksons Research, around 70% of vessels due for a special survey in 2025 were 15 years old or more — up from about 45% a decade earlier. Older ships need more steel renewal, more equipment replacement, and more class-driven remediation. Each survey visit at 20 years old typically costs two to three times what the same ship required at 10 years old.

The second is regulation. From 2019 onwards, three waves of environmental compliance work have hit the fleet in sequence. Scrubbers — sulfur oxide exhaust cleaning systems — were retrofitted onto roughly 5,000 ships between 2019 and 2023, driven by the IMO 2020 sulfur cap. Ballast water management systems were retrofitted onto more than 35,000 vessels ahead of the September 2024 compliance deadline. Both of those waves have now peaked. What replaces them in 2026 is shore power — the ability to plug into onshore electricity while alongside, avoiding auxiliary-engine emissions in port. FuelEU Maritime and the EU ETS, together with parallel requirements in California, China, and India, have created a rolling retrofit market that industry equipment suppliers expect to continue until at least 2030.

The third is energy efficiency itself. The IMO's CII framework — and the Net Zero Framework approved in principle at MEPC 83 in April 2025, with earliest entry into force in 2028 if adopted at the autumn 2026 review — both push older ships toward efficiency retrofits: new propellers, energy-saving ducts, hull modifications. The alternative is either a lower CII rating or, once NZF is in force, a compliance surcharge. Repair yards have found themselves handling both the regulatory work and the efficiency work in the same dock visit.

The result is a repair market that is close to fully booked at the top yards well into 2027, with lead times in some segments now stretching to 12 months.

Bottom line

The dry-dock cycle isn't glamorous, but it is one of the few genuinely predictable rhythms in shipping. Every ship comes back to a yard on a schedule set by regulation, does a carefully sequenced list of work, and leaves with a fresh certificate. In 2026 more ships than usual are on that cycle — the fleet has aged, the regulations have tightened, and the retrofit backlog is still working through — and the geography of where they go is narrower than it has ever been.

Three countries do half the work, one facility in Dubai handles most of the Middle East's tanker traffic, and the world's largest shipbuilder is quietly stepping back from ordinary repair work to focus on complex refits. The map is getting more concentrated, not less.

Sources

- IMO SOLAS Chapter I (Regulations 7, 10 — periodic survey requirements: intermediate and special)

- Clarksons Research (fleet age profile, special-survey volumes, dry-docking demand growth)

- TrustedDocks maritime intelligence platform (repair yard directory: 723 yards, 95 countries)

- Riviera Maritime Media / Cavotec (shore-power retrofit market drivers)