A class surveyor boards your vessel and asks for one thing before entering the engine room: the planned maintenance records. Not the engine itself. Not the logbooks. The PMS printout. Because if the maintenance system is in order, everything else is likely in order too. If it is not, the surveyor already knows what they will find below.

§1 — What PMS Is (and Why Every Ship Has One)

A Planned Maintenance System is exactly what the name describes: a structured schedule of maintenance tasks for every piece of machinery on board — main engine, auxiliary engines, boiler, steering gear, major auxiliaries like scrubbers, ballast water treatment systems (BWTS), refrigeration plant, air compressors, purifiers, and the pumps and valves that support them — organised by unique equipment IDs, triggered by running hours or calendar intervals, and documented in a form that a class surveyor can audit. It is not a software product — PMS is a requirement. The ISM Code, Section 10, mandates that every ship subject to SOLAS Chapter IX must maintain a documented system for identifying, planning, and recording maintenance of all equipment critical to safe operation.

The International Association of Classification Societies (IACS) recognises three approaches to machinery survey — the mechanism by which class societies verify that a vessel remains in a seaworthy condition. The classification survey cycle consists of annual surveys (every 12 months), an intermediate survey (at the 2.5-year mark), and a Special Survey (every 5 years) — the most comprehensive of the three. Under the traditional approach, the Special Survey concentrates all major machinery inspection into a single drydocking event. Continuous Survey of Machinery (CSM) spreads those inspections across the 5-year cycle, with the chief engineer and a class surveyor attending each item in turn. Planned Maintenance Survey (PMS) allows operators to demonstrate, through documented maintenance records, that equipment is being maintained to standard without waiting for a scheduled class visit. PMS is the most flexible — and most common — approach. Most of the global fleet operates on CSM or PMS today.

The three pillars of any PMS are the equipment register (every component from main engine down to the smallest critical pump, tagged and classified by criticality), the maintenance schedule (what needs to be done to each item and when), and the audit trail (who did it, what was used, what was measured, when it was completed). The third pillar is what surveyors actually read. Class credit is only granted when documentation is complete. A ship that maintains its machinery but does not document it has, from the surveyor's perspective, not maintained it at all.

§2 — What 40% of OPEX Buys (and Why Much of It Is Waste)

Maintenance is the largest single component of vessel operating expenditure — OPEX, in industry shorthand. Industry benchmarks from Drewry's Ship Operating Costs Annual Review consistently place it at approximately 40% of total daily OPEX — ahead of crew costs, insurance, and administration. Drewry's 2024 assessment put the global average daily OPEX across 47 vessel types at approximately $8,000, with significant variation by vessel type and age.

A 10-year-old Capesize bulk carrier (180,000 deadweight tonnes, DWT) typically runs at $7,000–8,000/day OPEX. A VLCC of similar age — at roughly 320,000 DWT — runs $9,000–11,000/day. A modern 14,000 TEU container ship sits in the $9,500–11,500/day range. An LNG carrier, with its cryogenic cargo systems and dual-fuel propulsion, can reach $13,000–16,000/day. Across all of these, repair and maintenance — combined with periodic drydocking — typically accounts for 35–45% of total daily OPEX.

Vessel age matters as much as vessel type. Drewry's data shows that maintenance costs for a 20-year-old vessel are typically 1.8 to 2.2 times those of a newbuild of the same type — driven by ageing machinery requiring more frequent overhauls, regulatory compliance retrofits (BWTS installation, scrubber fitting, IMO Tier III NOx emission systems), and increasing class survey scrutiny. By the time a vessel reaches its fourth special survey at 20 years, the maintenance burden is structural, not incremental.

The problem is not that maintenance is expensive. The problem is that a significant portion of it is premature. Under schedule-based PMS, components are overhauled at fixed intervals — the manufacturer's recommended hours or the class surveyor's cycle. A main engine exhaust valve might be scheduled for overhaul every 8,000 to 16,000 running hours depending on engine type, fuel, and operating profile. The cost of a cylinder head overhaul — parts, lubricants, labour, port time — varies significantly by engine model and bore size, typically ranging from $15,000 to $30,000 per cylinder for mainstream two-stroke designs. A typical two-stroke main engine has 6 to 8 cylinders for tanker and bulk carrier service, and up to 10 to 12 on the largest container vessels. If a single overhaul cycle is brought forward by several thousand hours because the schedule says so rather than because the valve needs it, the cost is real and the benefit is zero.

Across a fleet of 20 vessels, exhaust valve overhauls performed several thousand hours ahead of actual need can easily represent $2–4 million in unnecessary expenditure. Multiply that pattern across the full scope of scheduled maintenance: turbocharger overhauls, fuel injector renewals, piston ring inspections, bearing renewals, purifier disc cleaning, boiler tube inspections, scrubber pump overhauls. The cumulative waste is large. It is also invisible under current accounting: all of it shows up as normal maintenance cost, correctly documented and class-approved, entirely unremarkable.

§3 — What AI Changes (and What It Has Already Changed)

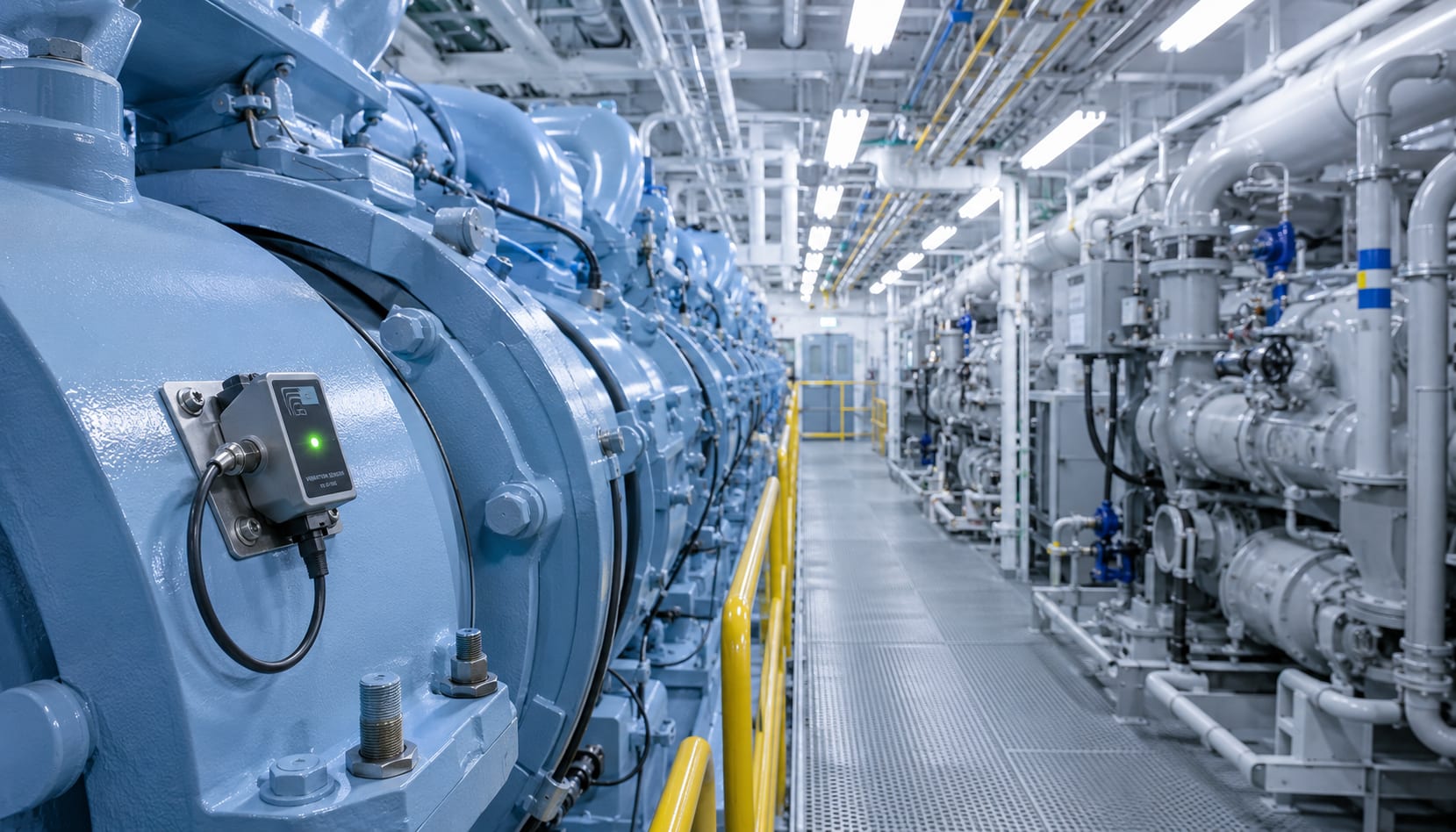

Predictive maintenance (PdM) replaces the schedule trigger with a condition trigger. Instead of overhauling at a fixed interval, the system monitors the condition of the component continuously — through cylinder pressure sensors, vibration monitoring, lube oil condition analysis, exhaust gas temperature readings, and turbocharger performance data — and flags maintenance only when the data indicates actual degradation. The maintenance action is deferred until it is genuinely needed, and performed before the component fails.

The largest predictive maintenance platforms in commercial shipping are operated by the engine manufacturers themselves — each monitoring its own installed base.

MAN Energy Solutions, whose two-stroke engines power approximately 80% of the world's ocean-going main propulsion, runs PrimeServ Assist — a 24/7 proactive monitoring service built on the MAN CEON cloud platform. PrimeServ Assist uses real-time sensor data, AI-driven diagnostics, and remote operating centres staffed by MAN engineers to detect anomalies before they become failures. TORM, one of the largest product tanker operators, is among the fleets using the service across its MAN-powered vessels.

Wärtsilä runs Expert Insight, covering its four-stroke and dual-fuel engine portfolio. The service combines on-board edge computing with shore-based analytics through a global network of Expertise Centres in Singapore, Houston, and Hamburg. In February 2025, Wärtsilä signed a Lifecycle Agreement with CMA CGM covering 14 LNG-fuelled container ships — five 15,000 TEU (twenty-foot equivalent unit) vessels and nine 23,000 TEU vessels — that includes Expert Insight monitoring for main engines, auxiliaries, and turbocharger management. NYK piloted the same service on two LNG carriers, Marvel Falcon and LNG Sakura, with the potential for fleet-wide deployment.

WinGD, the Swiss-Chinese two-stroke engine maker (formerly part of Wärtsilä, now owned by CSSC), operates WiDE — the WinGD Integrated Digital Expert — which monitors X-DF dual-fuel engines. WinGD piloted condition-based maintenance with Bernhard Schulte Shipmanagement on an LNG carrier powered by X72DF engines, estimating remaining useful life for cylinder liners, piston rings, exhaust valves, fuel pumps, and fuel injectors.

The architecture across all three is the same: on-board sensors collect data, edge computing performs initial analysis, and shore-based engineers validate the findings before sending specific maintenance recommendations to the crew. The technology stack is mature. The adoption numbers are not.

The barrier is acknowledged across the industry. Wärtsilä's Director of Fleet Optimisation, Markus Mannevaara, has acknowledged the gap publicly — the cost of installing and integrating IoT equipment and big data infrastructure, he notes, remains a barrier for many operators considering the transition. Other vendors have reached comparable deployment levels: Kongsberg Maritime's condition monitoring suite includes remaining useful life (RUL) estimation for thruster bearings; ABB Ability Marine Advisory System covers propulsion and power management; Kongsberg Digital's Kognifai platform adds fleet-wide analytics.

§4 — Why Most Ships Cannot Use It Yet

Approximately 300 vessels currently operate under AI predictive maintenance programmes. The global commercial fleet numbers around 60,000 vessels. The adoption rate is below 0.5%. This is not because shipowners are unaware of the technology or unconvinced by the results. It is because the economics do not work for most of the fleet.

Entry-level monitoring costs $15,000–50,000 per vessel per year, covering contract, sensor installation, connectivity, and the ongoing analytics service. For a single-ship operator running a 20-year-old Handysize bulker, that cost is not recoverable against the maintenance savings the technology would generate. The vessel does not have the sensor infrastructure the system requires. Retrofitting it costs more than the expected savings over the vessel's remaining commercial life.

The return-on-investment calculation illustrates the scale dependency. A mid-size operator with 20 modern vessels paying $30,000 per vessel annually for entry-level monitoring incurs $600,000/year in direct platform cost — before crew training, sensor retrofit, or connectivity. Against a typical fleet R&M (repairs and maintenance) budget of approximately $1.5 million per vessel (10-year-old Capesize at $7,500/day OPEX × 40% R&M share × 365 days), a 30% reduction on covered equipment categories represents roughly $450,000–$600,000 of avoided cost per vessel. Across 20 vessels, that is $9–12 million in annual savings — but only after the platform has matured past its 12–18 month baseline learning period, and only if the operator has the in-house capacity to act on the alerts. Smaller operators, with five vessels or fewer, often face the inverse: platform costs land before the savings, and the cash flow gap is what kills the business case.

For older vessels — those 10–15 years or above — the sensor deficit is structural. Modern newbuilds arrive with monitoring points built into the machinery as standard. A vessel built before roughly 2015 has very few of those monitoring points — often only basic alarms and a few pressure/temperature gauges feeding the engine control room. Installing full monitoring infrastructure means routing cable through machinery spaces, commissioning new instrumentation, integrating with existing alarm systems, and retraining crew. The capital cost alone can exceed $100,000 per vessel for a full engine monitoring suite.

AI models also need time. A machine learning system trained on exhaust valve behaviour patterns from one class of engine will not perform well on a different class. Each deployed vessel contributes to model improvement, but a newly connected vessel typically requires 3–6 months of baseline data collection before the system can reliably distinguish degradation from normal operating variation. For operators rotating vessels between trades, that baseline is constantly disrupted.

The fourth barrier — crew trust — is real but often overstated. Chief engineers with 25 years of experience on the same engine type have valid grounds for scepticism when an algorithm tells them to overhaul a bearing the engineer has judged as serviceable. The systems that have succeeded have addressed this through the human expertise layer: the alert goes to a shore-based engineer first, who validates the finding and provides a specific recommendation the crew can evaluate on its own merits. The dividing line is not capability. It is scale.

§5 — People — Skills the System Needs, Skills the Industry Has

The technology stack assumes the crew can use it. That assumption is increasingly under pressure.

The Standards of Training, Certification and Watchkeeping for Seafarers (STCW) — the IMO convention that governs what every officer must be qualified to do — was established in 1978 and last substantially amended at the 2010 Manila Conference. It does not contain explicit competency standards for sensor data interpretation, anomaly detection, predictive analytics, or cybersecurity. The IMO's 2021 regulatory scoping exercise for Maritime Autonomous Surface Ships (MASS) identified these gaps formally. As of mid-2026, no IMO instrument requires a Chief Engineer to be able to read a turbocharger vibration spectrum or validate an AI-generated maintenance recommendation.

The skills that predictive maintenance requires in practice include:

- Interpreting sensor data trends — distinguishing between equipment degradation, sensor drift, and false positives from operational variation

- Validating shore-based AI recommendations against on-ship observation — the alert says "renew bearing X," but does the crew agree?

- Operating digital twin interfaces — a 3D model of the engine room that may have been built by the yard but maintained by the operator

- Cybersecurity awareness — the same data link that enables predictive maintenance is also the attack surface a hostile actor could exploit

- English-language technical reporting — most shore-side analytics teams operate in English, regardless of the vessel's flag

In parallel, the role of the Electro-Technical Officer (ETO) — created in the 2010 STCW amendments — has become a structural bottleneck. ETOs handle the electrical and electronic systems that predictive maintenance depends on. The global supply of qualified ETOs has not kept pace with the digitalisation of newbuilds. BIMCO and ICS manning reports through 2024 and 2025 have flagged ETO shortages as one of the most acute officer-rank gaps, alongside senior engineering officers more broadly.

The on-ship reality is also a generational question. The current global pool of Chief Engineers entered training when PMS was the leading edge of digitalisation. Many will retire before predictive maintenance becomes mainstream. The Chief Engineers who will run AI-monitored ships in 2035 are currently cadets — and the maritime academies training them are still updating their curricula. Some institutions, particularly in the Nordic countries and Singapore, have introduced data analytics and digital twin modules. Most have not.

The practical implication is that operators deploying predictive maintenance face a parallel investment: not just the sensors and the analytics platform, but the people who can use them. For large fleet operators, this means dedicated digital-shipboard training programmes, shore-based engineer rotations that build cross-platform expertise, and partnerships with academies and class societies. For smaller operators, it often means the technology is available but the human capacity to extract value from it is not.

The dividing line between successful and unsuccessful predictive maintenance deployments is rarely the algorithm. It is whether the Chief Engineer trusts what the algorithm tells him — and whether his training, his time, and his contract give him a reason to engage with it.

§6 — Where This Goes (and Why the Timeline Matters)

The ship repair and maintenance market is valued at approximately $32 billion globally as of mid-2026, with projections to $60.6 billion by 2035. The digital twin market in marine applications — currently around $0.59 billion — is projected to reach $2.40 billion by 2032, a compound annual growth rate of 23.2%. That is nearly four times the growth rate of the broader maintenance market. The divergence tells you where the investment is flowing. These are large numbers, but what matters more than the headline figures is what drives the growth.

The first driver is the newbuild cycle. Vessels currently under construction at Korean, Japanese, and Chinese yards are being specified with IoT sensor packages as standard. A 2024 newbuild LNG carrier arrives with hundreds of monitoring points already integrated. By 2030, the share of the fleet with native monitoring capability will be materially larger than it is today — not because owners retrofitted older ships, but because the new ships replaced them.

The second driver is regulatory. The EU Emissions Trading System (EU ETS) entered full implementation for shipping in 2026, and the UK Emissions Trading System (UK ETS) followed. Under both frameworks, fuel consumption directly drives carbon cost. An engine running beyond its optimal condition — slightly elevated fuel consumption, degraded combustion efficiency, elevated exhaust temperatures — is not just a maintenance problem. It is a carbon compliance problem. Every percentage point of fuel efficiency lost to deferred or incorrect maintenance now has a regulatory price attached to it. Predictive maintenance, in this context, is not just about reducing OPEX. It is about reducing the EU ETS invoice.

The third driver is the class society framework. The International Association of Classification Societies (IACS) is evaluating how AI-generated maintenance data can substitute for or supplement traditional survey evidence. DNV has already moved fastest among the major societies — its "Smart" class notation, introduced in 2022 and expanded in 2024 and 2025, recognises vessels with integrated condition monitoring and provides a framework for reduced physical inspection of monitored systems. Lloyd's Register, ABS, and Bureau Veritas have parallel programmes at various stages of maturity. If a vessel can demonstrate, through continuous sensor data and validated expert analysis, that a component has been maintained to standard, the argument for requiring a physical class survey of that component weakens. By 2028, it is likely that at least one major class society will publish guidelines for accepting AI maintenance evidence in lieu of scheduled survey items. When that happens, the economics of predictive maintenance improve substantially for the vessels that already have it deployed.

The log the surveyor reads first is getting smarter. The question is whether your fleet is getting smarter with it.