In 1855, a group of British shipowners solved a problem that conventional insurers refused to touch.

Hull and machinery insurance — covering the ship itself — had existed for centuries. Lloyd's of London would insure the vessel. What insurers would not cover on commercially viable terms were the third-party liabilities that a ship could create: injury and death among the crew, damage to cargo carried for hire, pollution, collision damage to other vessels, and the cost of removing a wreck from a fairway. These liabilities were open-ended, potentially enormous, and accumulated in ways that no actuary could reliably price in advance.

The shipowners' solution was to insure each other. They formed a club — a mutual association in which every member both pays into the pool and draws from it when a claim arises. No outside shareholders. No guaranteed profit margin. Premiums, called calls, are set at whatever level is needed to cover the claims that actually occurred. If a bad year produces large claims, members pay a supplementary call. If claims are lower than expected, the surplus rolls forward.

Think of it as a neighbourhood where every homeowner pays into a shared fund — when one house floods, the fund pays. Nobody is trying to make money from the arrangement.

That model — Protection and Indemnity — has operated continuously since 1855. The clubs that run it today cover approximately 90% of the world's ocean-going tonnage. Every tanker, bulk carrier, container ship, and general cargo vessel you see moving through a port almost certainly has a P&I certificate behind it.

What P&I insurance covers — and what it does not

The name divides the coverage into two categories. “Protection” covers liabilities arising from the ship's operation involving people. “Indemnity” covers liabilities arising from cargo, property, and environmental damage. The boundary is not always intuitive, but the principle is consistent: P&I covers third-party liability. It does not cover the ship itself.

Hull and machinery (H&M) insurance, which covers the physical vessel, is purchased separately — typically from commercial marine insurers. The two policies are complementary: H&M pays for the ship; P&I pays for what the ship does to everything else. A shipowner operating without both is not fully protected, and most charter party contracts, port state requirements, and flag state regulations require evidence of P&I cover as a condition of operation.

The mutual model — no shareholders, no profit motive

A P&I club is constituted as a mutual association, not a limited liability company. The members are the owners. Each shipowner registers — or “enters,” in P&I terminology — their vessels with a club, and in return gains the right to draw on the pool if a covered claim arises. Annual premiums, called advance calls, are set by the club's board based on projected claim costs. If actual claims exceed projections, a supplementary call is levied on the membership in proportion to their entered tonnage.

This structure has practical consequences that distinguish P&I from commercial insurance. Claims are handled on a cost-recovery basis rather than a profit-maximisation basis. The club's interest is to resolve claims fairly and efficiently, because unresolved claims accumulate as liabilities against the whole membership. A commercial insurer that underestimates a risk loses its own capital. A P&I club that underestimates a risk distributes the shortfall across its shipowner members at the next supplementary call.

The other consequence is the “pay to be paid” rule embedded in most club rules: a member must actually pay the third-party claimant before the club reimburses the member. This prevents the club from being drawn into disputes between owners and claimants where the member has not yet accepted liability. It also means that a member with a legitimate claim who cannot fund the initial payment may face a financing problem — one of several practical limitations the mutual structure imposes on smaller operators.

The twelve clubs

The International Group of P&I Clubs (IG) is the umbrella body that coordinates the pooling agreement and collective reinsurance programme. Twelve clubs currently hold IG membership. Seven of the twelve are based in the United Kingdom.

- American Club (New York)

- Britannia (London)

- Gard (Arendal / Oslo)

- Japan P&I Club (Tokyo)

- London Club (London)

- NorthStandard (Newcastle / London — formed in February 2023 from the merger of North P&I and Standard Club)

- Shipowners' Club (London)

- Skuld (Oslo)

- Steamship Mutual (London)

- Swedish Club (Gothenburg)

- UK Club (London)

- West of England (London)

Until February 2023, there were thirteen clubs. North P&I and Standard Club merged that year to form NorthStandard, reducing the total to twelve. The list is not static — but the architecture is.

Membership in the IG is the defining distinction between mainstream P&I and everything else. Non-IG clubs exist, and some fixed-premium P&I products are available from commercial insurers, but IG membership confers access to the pooling and collective reinsurance programme — the mechanism that allows even a medium-sized club to back a $3 billion claim. Without IG membership, a club's coverage ceiling is limited to its own reinsurance arrangements, and the capacity gaps become significant when major casualties occur.

The clubs between them cover approximately 90% of the world's ocean-going tonnage and 95% of all tankers. For an understanding of how P&I interacts with ship classification and flag state compliance, see our explainer on Classification Societies.

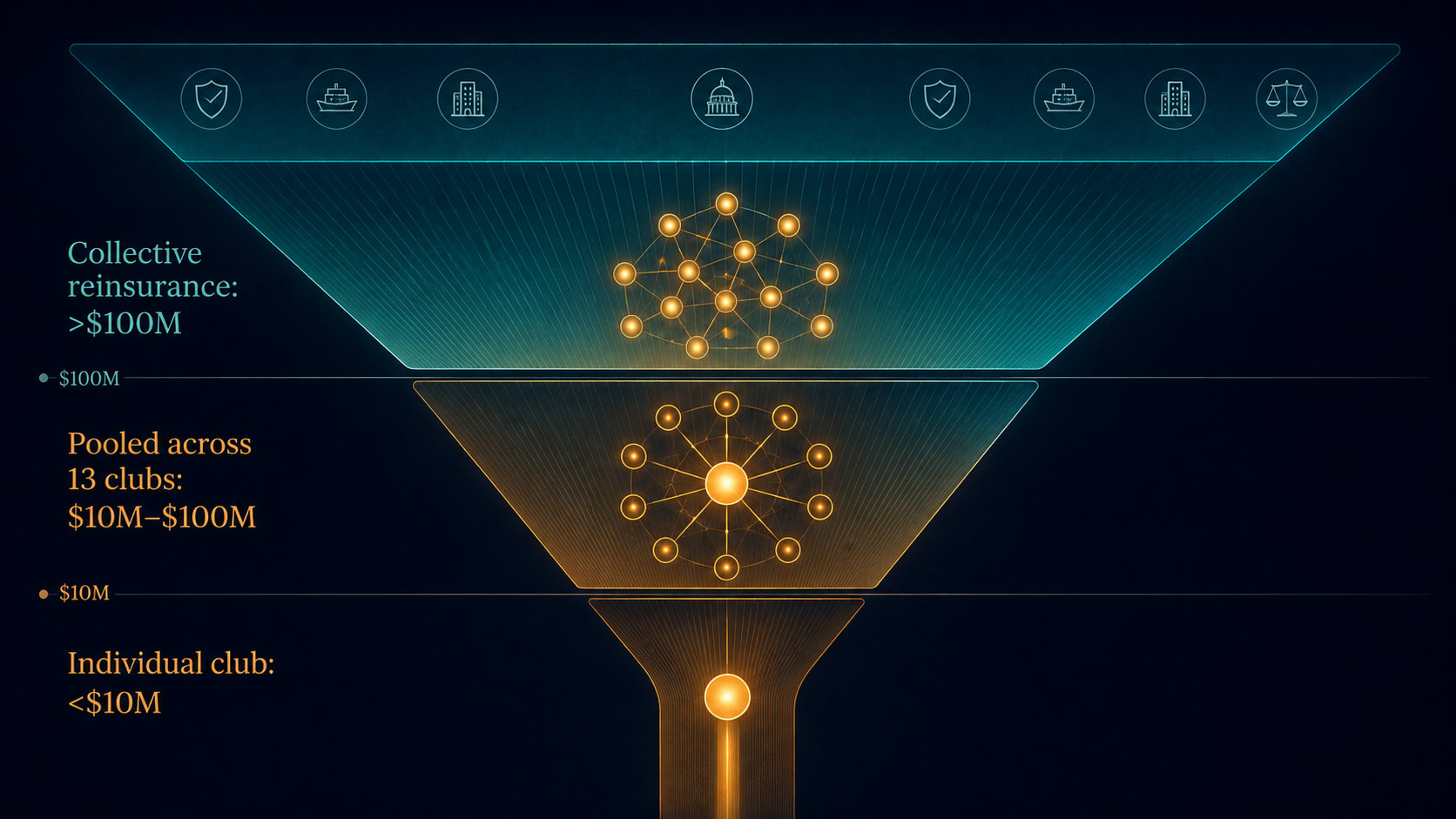

How a $3.35 billion claim gets paid

The pooling and reinsurance architecture of the IG is the most important — and least understood — part of the P&I system. It is the mechanism by which a single catastrophic claim that would overwhelm any individual club is distributed across the entire mutual.

The structure operates in five layers:

Layer 1 is the individual club's own retention. Claims up to $10 million are paid from the entering club's own funds. No other club is involved.

Layer 2 is the pool. Claims between $10 million and $30 million are shared across all twelve clubs in proportion to their entered tonnage. A large claim against a small club does not fall entirely on that club's members — it is distributed across the entire IG membership.

Layer 3 is Hydra. Above $30 million, up to $100 million, the claim is reinsured by Hydra Insurance Company Limited — a captive reinsurance vehicle incorporated in Bermuda and owned collectively by the twelve clubs through segregated accounts. Hydra is not a commercial reinsurer; it is the IG's own reinsurance vehicle, structured to give the clubs direct control over this layer of coverage.

Layer 4 is the Group Excess Loss programme (GXL). Above $100 million, the IG purchases commercial reinsurance from the open market, structured in three sub-layers that collectively extend coverage to approximately $2.25 billion above the Hydra layer. This is the layer where Lloyd's syndicates, global reinsurers, and capital market vehicles participate.

Layer 5 is the Collective Overspill. Above the GXL ceiling, the twelve clubs together bear one final $1 billion layer of shared liability — a backstop that, in practical terms, has never been exhausted.

The total ceiling is approximately $3.35 billion per incident. It is the largest concentration of mutual liability cover in any single industry on the planet.

The legal requirement

For most vessels carrying oil in bulk, P&I cover is not optional. It is a legal requirement under two international conventions.

The Civil Liability Convention (CLC 1969, substantially revised by the 1992 Protocol) requires shipowners carrying persistent oil in bulk to hold compulsory insurance for pollution liability up to limits defined by vessel tonnage. The insurer must issue a certificate of financial responsibility — the “blue card” — that can be presented to port state authorities on demand. A vessel entering a port that is party to the CLC without a valid blue card can be detained.

The supplementary layer is provided by the IOPC Funds, established by the 1971 Fund Convention and strengthened by the 1992 protocols. Where a pollution claim exceeds the shipowner's CLC limit — or where the shipowner is insolvent or unidentifiable — the IOPC Fund compensates claimants up to a higher ceiling, funded by contributions from oil importers in member states. The P&I club provides the first response; the IOPC Fund provides the overflow.

Beyond tankers, port state authorities in most major jurisdictions require evidence of P&I cover for any vessel calling at their ports. The legal framework varies — some rely on the CLC, others on domestic port regulations — but the practical result is the same: without IG P&I cover, a vessel's ability to trade commercially is severely restricted.

When the architecture is tested

The pooling and reinsurance system was designed after experience proved that individual club capacity was insufficient for the largest marine casualties. The 1967 grounding of the Torrey Canyon — the first supertanker casualty, which released 119,000 tonnes of crude oil off the coast of Cornwall — exposed gaps in both the insurance architecture and the legal framework that took years to repair. The IG pool was restructured in its aftermath, and the international CLC and Fund Convention framework that followed was a direct legislative response to the Torrey Canyon's unresolved liability questions.

The most recent stress test came in March 2024, when the container ship Dali lost power and struck the Francis Scott Key Bridge in Baltimore, causing the bridge to collapse and killing six construction workers. The vessel was entered with NorthStandard. Total insured losses were estimated at up to $4 billion — potentially the most expensive marine casualty on record. The claim activated the full IG architecture: NorthStandard's individual retention, the pool with Hydra reinsurance, and the GXL layers above. The system absorbed it. The scale of the Baltimore loss — bridge reconstruction, port closure, cargo salvage, wrongful death claims — demonstrated that the pooling structure designed after Torrey Canyon in 1967 could handle a twenty-first century catastrophe.

The Dali claim is also a reminder of why NorthStandard's formation matters structurally. When North P&I and Standard Club merged in February 2023 — eleven months before the Baltimore incident — they created one of the largest clubs in the IG by entered tonnage, with a correspondingly larger stake in the pool. A claim of this magnitude handled by a smaller club would have drawn proportionally more from the shared pool. NorthStandard's scale meant more of the initial retention was absorbed within a single, financially robust entity before pooling was triggered.

The commercial passport

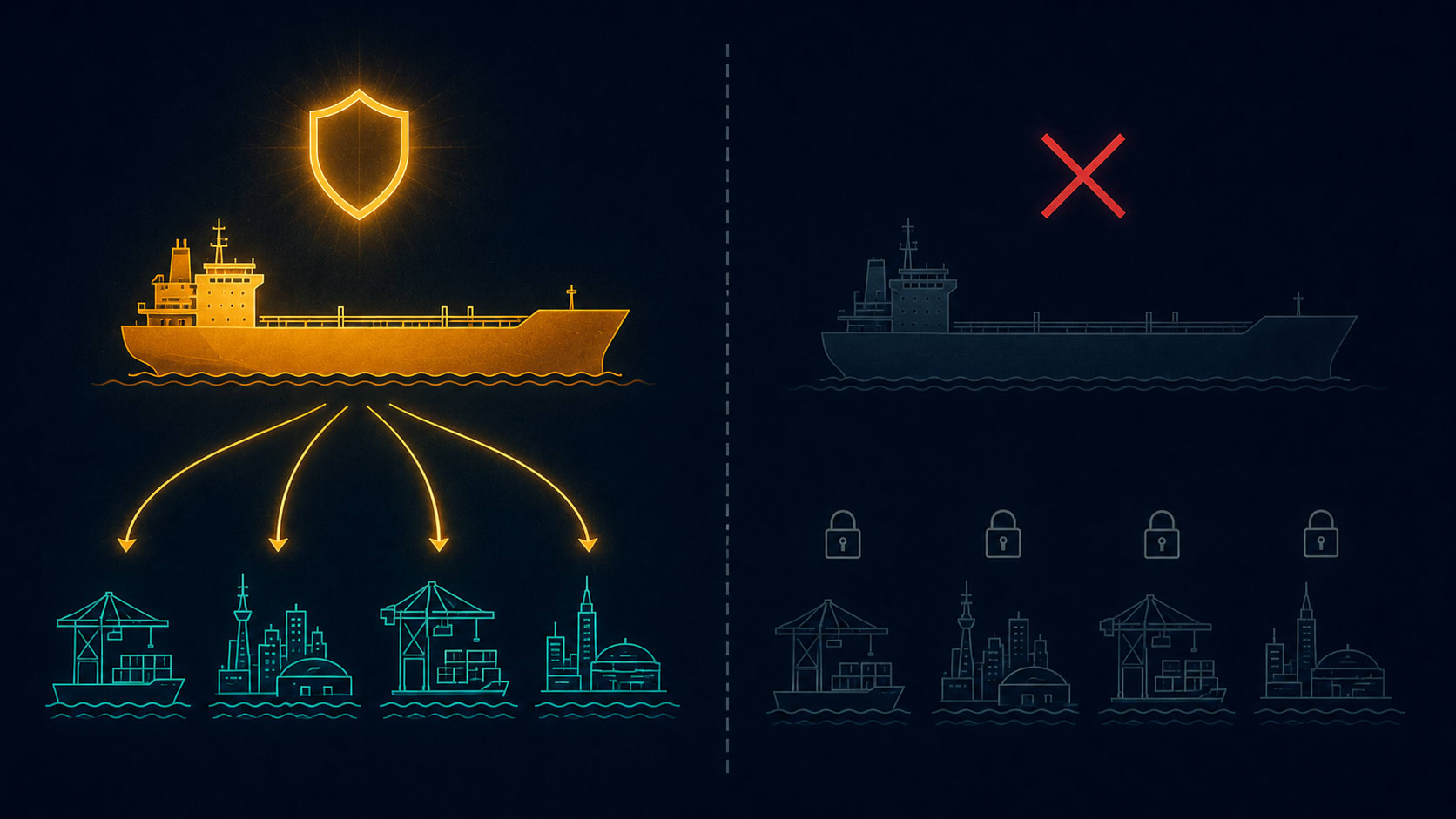

P&I cover has evolved from an insurance mechanism into a market access requirement. Ports, flag states, charterers, and financiers all use IG P&I membership as a proxy for a vessel's commercial legitimacy and financial standing.

The vessel operating outside the IG P&I system — typically because it is sanctioned, operating under a flag with no CLC obligations, or registered with a non-IG mutual — faces concrete commercial consequences. Major oil company vetting programmes (SIRE for tankers, CDI for chemical tankers) require evidence of IG P&I cover. Most time charter contracts contain P&I warranty clauses. Port state control officers in Europe, Australia, and the Americas routinely check blue cards. Vessels without them can be detained, fined, or refused entry.

This is the mechanism by which the shadow fleet — the roughly 200 or more VLCCs and several hundred product and crude tankers operating on sanctioned trade — is effectively excluded from mainstream commerce. The vessels are still physically capable. They still carry cargo. But they cannot enter Rotterdam, Singapore, or Houston on normal commercial terms, because their P&I position disqualifies them from the networks that mainstream trade requires. For more on the shadow fleet's structural role, see our analysis of The Two Maps of Maritime Labour, and the VLCC Fleet Deep Dive on how the IG P&I insurance system intersects with effective fleet supply.

As of mid-2026, the clubs are actively recalibrating war coverage following escalation in the Strait of Hormuz — the IG's aggregated sublimited cover for excluded territories increased from $100 million to $125 million for the 2026/27 policy year. The architecture is not static. It recalibrates to geopolitical reality each renewal cycle.

For vessels that do carry IG P&I cover, the club relationship extends beyond claims handling. Most clubs provide legal assistance, correspondent networks in major ports, advice on flag state and port state requirements, and support during cargo disputes that have not yet become formal claims. The club's network of correspondents — local lawyers and surveyors in ports worldwide — functions as an operational support infrastructure that shipowners access as part of their membership.

The P&I structure is also relevant to charter party negotiations. Time charter contracts typically contain a warranty from the shipowner confirming that the vessel is entered with an IG P&I club and that cover will be maintained throughout the charter period. A breach of that warranty — if the owner allows the P&I entry to lapse — gives the charterer grounds to terminate. P&I cover is not just a condition of port access. It is a contractual commitment that defines the commercial relationship between owner and charterer.

The system that began with a group of British shipowners in 1855 now backstops the entire architecture of international maritime commerce. The twelve clubs of the International Group do not advertise. They do not compete on price in the way that commercial insurers do. They do not produce dividends. What they produce is the $3.35 billion ceiling — the assurance that when the next Dali-scale event occurs, the system will absorb it, and the ships will keep moving.

For the role of P&I in the context of ship classification and flag state compliance, see Classification Societies Explained. The interaction between P&I cover and charter party contracts is covered in Charter Parties Explained. For the shadow fleet's structural exclusion from IG P&I, see The Two Maps of Maritime Labour and the VLCC Fleet Deep Dive.