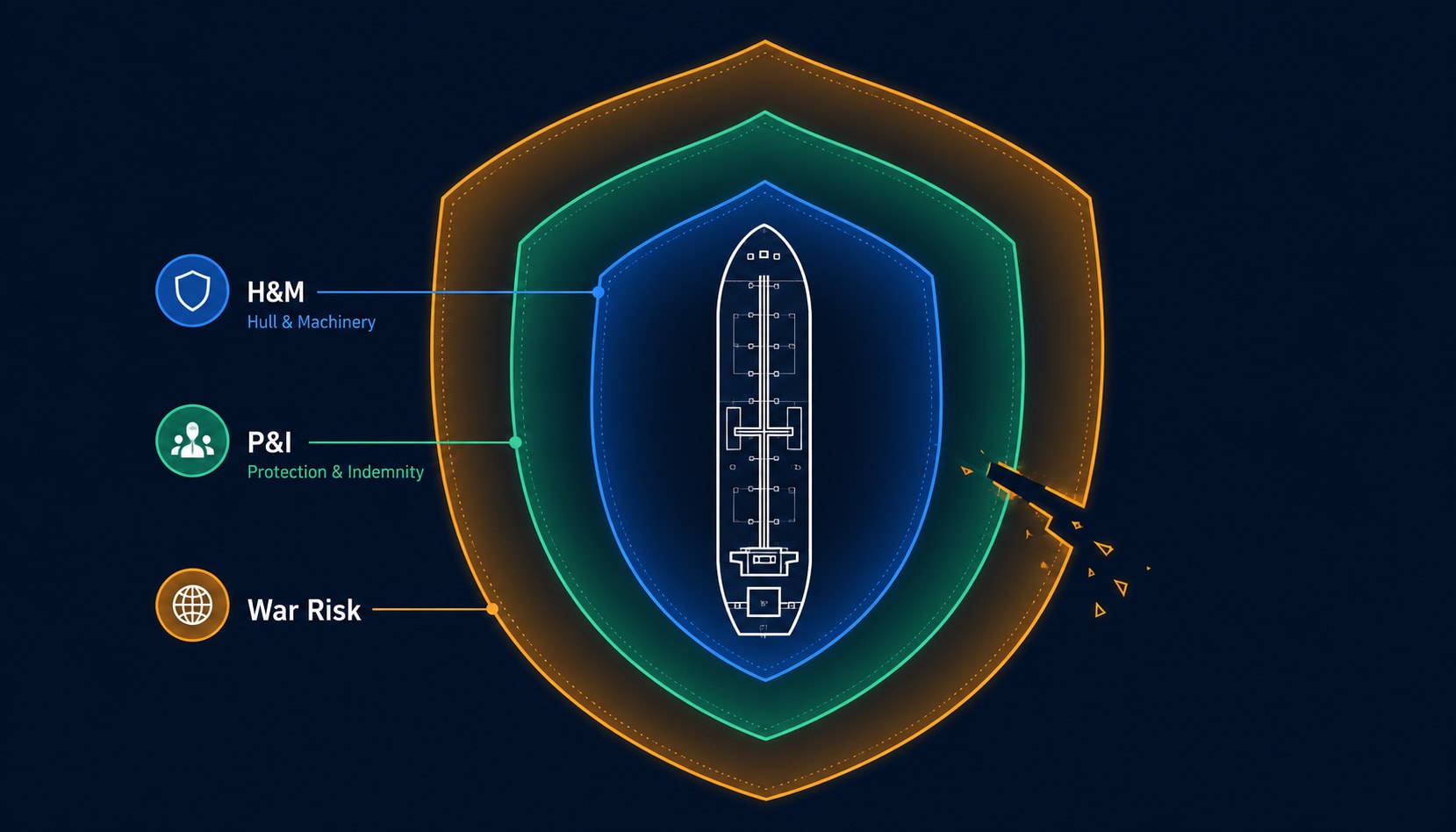

§1 — Hull & Machinery: The Ship Itself

Hull & Machinery (H&M) insurance covers the physical structure of the ship — its hull, engines, boilers, machinery, and equipment. It is the maritime equivalent of a property insurance policy, and it operates under commercial terms negotiated annually between the shipowner and an insurer, at Lloyd's of London, the London company market, or through major hull underwriters in Europe, Norway, Japan, and the United States.

The H&M policy covers physical damage caused by perils of the sea — collisions, groundings, storms, fire, explosion, and similar events. What it does not cover, by default, is the liability arising from damage the ship causes to third parties. That is where P&I begins.

One detail that surprises most people unfamiliar with shipping: the 3/4 collision clause. When a vessel collides with another ship, H&M covers three-quarters of the shipowner's liability to the other vessel. The remaining quarter falls to P&I. This split dates to nineteenth-century London market practice and has never been renegotiated out of existence. It is now so embedded in shipping finance that lenders require both policies simultaneously — H&M for the asset, P&I for the liability gap the H&M policy deliberately leaves open.

§2 — P&I: The Club That Covers Everything Else

Protection & Indemnity insurance covers the shipowner's liabilities to third parties. This includes injury or death of crew and passengers, damage to cargo carried on board, oil pollution, wreck removal, and the remaining quarter of collision liability that H&M deliberately excludes. P&I also covers the costs of crew repatriation, port state detention, and a range of other liabilities that can make a voyage catastrophically expensive if they are uninsured.

The International Group (IG) consists of twelve P&I clubs — including Gard, Britannia, the American Club, Japan P&I, and Steamship Mutual — that collectively insure approximately 90 percent of the world's ocean-going tonnage. P&I clubs are mutual organisations: members are both the insured and the insurer. Premiums are called calls, and if claims exceed estimates, clubs issue supplementary calls to cover the shortfall.

The IG operates a pooling system for large claims. Claims up to approximately $10 million are retained by the individual club. Claims between $10 million and $100 million are shared across all twelve clubs through the pool. Above $100 million, the pool accesses reinsurance with a total capacity of approximately $3 billion.

A critical point about P&I and the Hormuz crisis: core P&I liability cover is non-cancellable. During the crisis, a number of fixed-premium charterer's P&I covers — written outside the mutual structure by commercial underwriters — were cancelled and mostly repriced. But the mutual system itself continued to function. The LMA confirmed in March 2026 that “liability coverage through the P&I Clubs is non-cancellable and remains reinsured in the London market.” The effect was still significant — additional war P&I exposure for Gulf transits became substantially harder and more expensive to assemble. But the mutual system did not fail.

§3 — War Risk: The Policy That Reprices Straits

War risk insurance covers losses arising from war, civil war, terrorism, piracy, strikes, and related perils that standard H&M and P&I policies explicitly exclude. It is priced separately because its exposure is fundamentally different — it tracks geopolitical events rather than maritime accidents, and can move from negligible to catastrophic in hours.

Lloyd's of London has long been the dominant global hub for marine war risk underwriting. The standard benchmark is the Annual War Risk Premium (AWRP), which for most routes runs between 0.1 and 0.2 percent of hull value per year for a modern, well-maintained tanker. In December 2025, Hormuz premiums were in that range — roughly $100,000 to $200,000 annually on a VLCC insured at $100 million.

When the February 2026 strikes closed the strait, the LMA surveyed Lloyd's marine war participants. Eighty-eight percent retained appetite to underwrite hull war risks. More than 90 percent retained appetite for cargo. The London market did not close. It repriced. Safer vessels with no US nexus were quoted around 1 percent within 48 hours. Mid-risk profiles drew 3 to 5 percent. US-nexus tankers and higher-risk profiles received quotes of 7 to 10 percent by mid-March, with some underwriters declining specific risks entirely.

The American P&I Club summarised the situation clearly: “The London market did not fail. It repriced.” But repricing at that scale has the same operational effect as withdrawal. A 10% annual premium on a $100 million hull value vessel is $10 million — before any additional voyage premium for the transit itself. Most voyage economics cannot absorb that cost and remain commercially viable.

The strait was commercially repriced before the mines were laid. War risk cover remained available throughout — but at premiums that made most voyages economically unviable. Combined with safety concerns assessed by masters and owners, the result was the same as a physical closure.

On June 19, 2026, Lloyd's launched a $400 million war risk consortium — $200 million for hull and P&I coverage, $200 million for cargo — led by Chubb. The consortium signals that Hormuz traffic is resuming, but its capacity covers approximately one day of cargo flow through the strait at Brent crude around $80 per barrel: roughly $1.6 billion of daily cargo value transiting a waterway the consortium covers in total.

§4 — How the Three Policies Interlock

The three policies are not independent. They interlock in a sequence that determines whether a commercial voyage is possible.

Think of the three policies as three stamps on a passport. H&M stamps the ship as seaworthy. P&I stamps it as financially responsible. War risk stamps the route as insurable. A port authority checks all three before granting entry. Miss one stamp and the ship anchors outside — intact, crewed, loaded, and going nowhere.

No H&M cover means the vessel's lender will accelerate the loan and the ship cannot be financed. No P&I entry means the vessel will not be permitted entry to most commercial ports — port state control requires P&I as a condition of entry. No war risk means the vessel cannot be chartered for routes that cross a Joint War Committee (JWC) listed area, because most charter parties explicitly require war risk coverage for listed zones, and no cargo insurer will insure the cargo aboard.

Charter parties allocate the cost of war risk between owner and charterer under standard BIMCO clauses. The baseline war risk premium is typically owner's account; any additional premium arising from the charterer's nominated voyage — where the charterer directs the vessel into a JWC-listed area — falls to the charterer. During the Hormuz crisis, charterers faced the choice of paying the additional war risk premium themselves or abandoning the fixture.

The shadow fleet operates outside this system. Approximately 200 VLCCs trading sanctioned crude hold no IG P&I, their H&M cover is either lapsed or placed with non-standard markets, and they carry no standard war risk. They continued transiting Hormuz precisely because they had no insurance system to constrain them. The mechanism that stopped mainstream commercial shipping — repriced war risk — had no purchase on a fleet that had already exited the insurance system.

§5 — What This Means for Shipping Economics

The cost impact of insurance on a single VLCC voyage illustrates why the repricing mechanism is so powerful. A fully loaded VLCC on the Middle East Gulf to China route (TD3C) at $95,000 per day earns approximately $5.7 million over a 60-day round voyage. Insurance costs on a normal route — H&M, P&I, and standard war risk — run to approximately $200,000 for the voyage.

A war risk premium of 3% on a $100 million hull value vessel adds $3 million for a 365-day annual premium, or approximately $490,000 for a 60-day voyage — more than twice the entire normal insurance cost. At 7%, the additional cost for the voyage runs to $1.15 million. At 10%, it approaches $1.65 million. These numbers do not make the voyage impossible. They make it substantially more expensive, shift the freight market, and compress margins to the point where most charterers and owners re-evaluate whether the route is worth taking.

This is the mechanism that explains why insurance is not a passive cost. It is an active constraint on trade. A navy takes weeks to deploy. A war risk premium can be repriced in hours. The repricing of a single strait rewrites the freight rate for every voyage touching that geography.

The Lloyd's $400 million consortium, launched June 19, is a market signal — not a market solution. At $1.6 billion of daily cargo value flowing through Hormuz at normalised volumes, the consortium covers roughly one day of that flow. Its significance is not its capacity. It is the statement that Lloyd's leading underwriters still have appetite to write this risk at commercially viable premiums, and that Hormuz business is open again. That signal is what moves the freight market — not the dollar amount.

Insurance is not a passive cost of doing business. It is an active constraint on trade — a system that can reprice a shipping lane faster than any navy, and that sets the floor under freight rates long after the geopolitical trigger has been resolved.

- Lloyd's of London / LMA, Marine War Risk Consortium announcement and market statement (March–June 2026)

- International Group of P&I Clubs, pooling and reinsurance structure documentation

- Argus Media, “Explainer: War risk insurance and AWRP” (March 10, 2026)