The strait opened on a Wednesday. By Saturday it was closed again. In between, twenty-five ships moved through a waterway that used to handle a hundred a day. More than one hundred days of disruption produced the largest coordinated reserve release in IEA history — and it was not enough.

The Hormuz crisis of 2026 has generated a category of analysis that might be called the geopolitics of reopening — what happens to oil prices when the blockade lifts, what happens to tanker rates when stranded vessels re-enter the market, what happens to insurance premiums when the zone reclassification is reversed. That analysis is useful. It is also partial. It treats the crisis as an interruption to a normally functioning system rather than as an exposure of that system's underlying structure.

The underlying structure is this: oil is still the operating system of the global economy, and ships are still the only way to run it. Hormuz did not change this. It demonstrated it — three times, in one hundred days, each time the strait closed again.

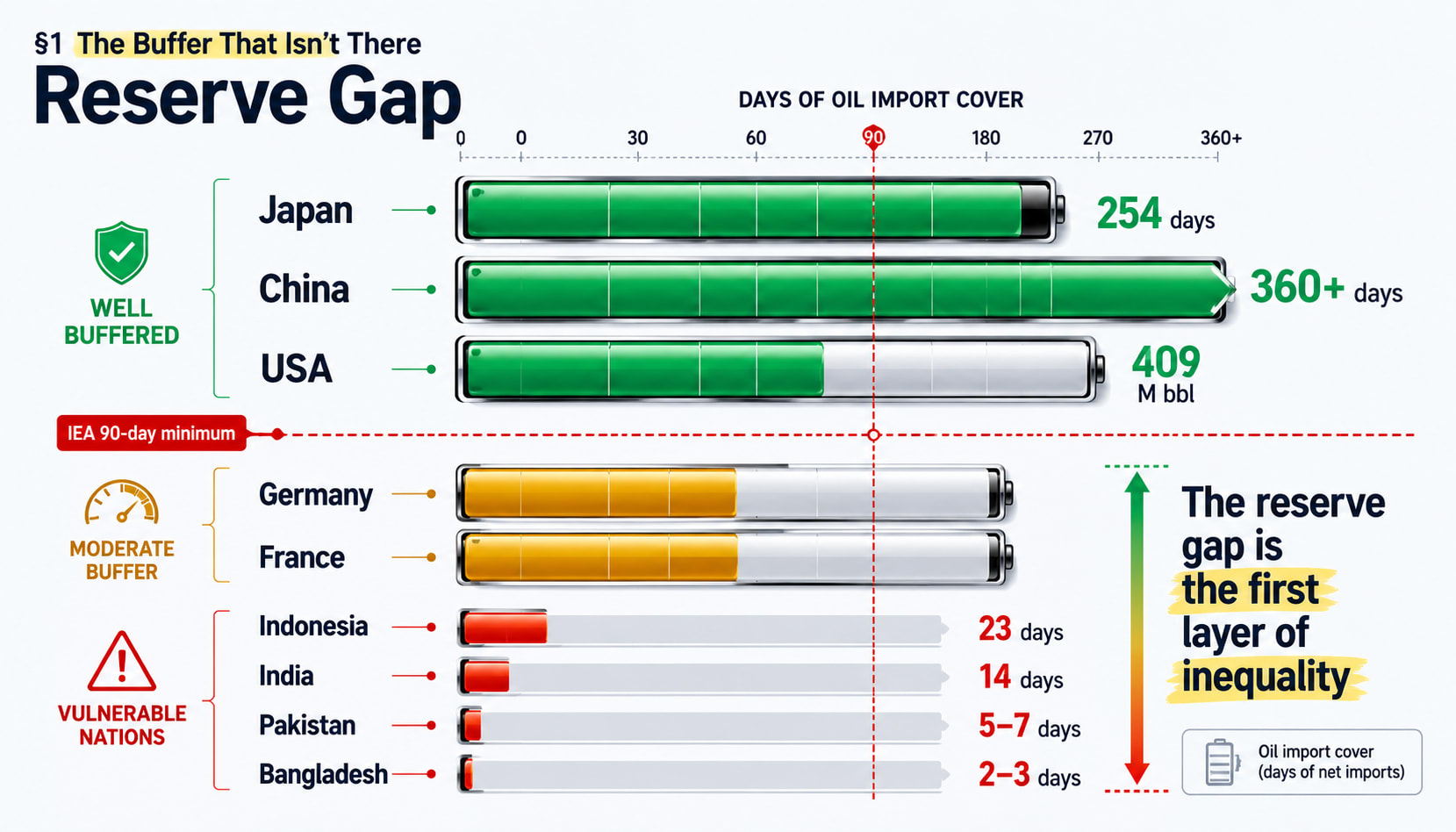

§1 — The Buffer That Isn't There

On March 14, the IEA authorized the largest coordinated emergency oil stock release in the organisation's history: 400 million barrels across member countries. For context, the 2022 response to Ukraine was 182 million barrels — the previous record. The 2026 decision was 2.2 times that figure. It covered approximately four days of global production.

The US Strategic Petroleum Reserve stood at approximately 409 million barrels as of April 2026, after an initial emergency exchange of 45.2 million barrels from the February level of roughly 415 million. The SPR was designed in 1975 as a buffer against a supply interruption lasting weeks. A closure that endured for more than one hundred days — and closed three times — was not the scenario the architecture was built for.

The reserve gap chart above is the first structural inequality the crisis exposed. Japan holds 254 days of net import cover. The United States holds roughly 200. Germany, at approximately 100 days, sits just above the IEA's 90-day minimum. Indonesia, India, and Pakistan hold 23, 14, and 5 days respectively. These are not temporary shortfalls. They are the permanent condition of oil-dependent economies that never built the infrastructure to survive a sustained supply interruption.

When Hormuz closed, the reserve gap did not create the crisis. It determined who felt it first — and how hard.

§2 — AI Does Not Replace Energy

The second structural exposure is the one that most energy analysis misses: the physical dependency of the AI economy on hydrocarbon supply chains.

Artificial intelligence is described as a software revolution, a digital transformation, an information technology paradigm. Those descriptions are accurate at the level of products and services. At the level of infrastructure, AI is an energy demand story. The IEA projects that AI data centres will add approximately 6.1 billion cubic feet per day of US natural gas consumption by 2030. That gas, when it does not serve domestic power generation, moves as LNG through export terminals in Louisiana and Texas, onto LNG carriers, and through the Strait of Hormuz to customers in Asia and Europe.

The dependency is not abstract. In 2025, 93 percent of Qatar's LNG exports and 96 percent of the UAE's LNG exports transited the Strait of Hormuz — together representing nearly one-fifth of global LNG trade. There are no alternative pipeline routes, no bypass infrastructure, no overland options. When Hormuz closed, those volumes did not reroute. They stopped.

A data centre that runs on electricity generated from natural gas that was once Qatari LNG is a data centre whose energy supply ships its output through the Strait of Hormuz. The AI economy is not separate from the physical supply chain. It is one more layer of demand stacked on the same bottleneck the world has failed to route around since 1970.

The 6.1 bcf/day projection applies to 2030. The dependency loop exists today. The crisis demonstrated what happens when the bottleneck closes.

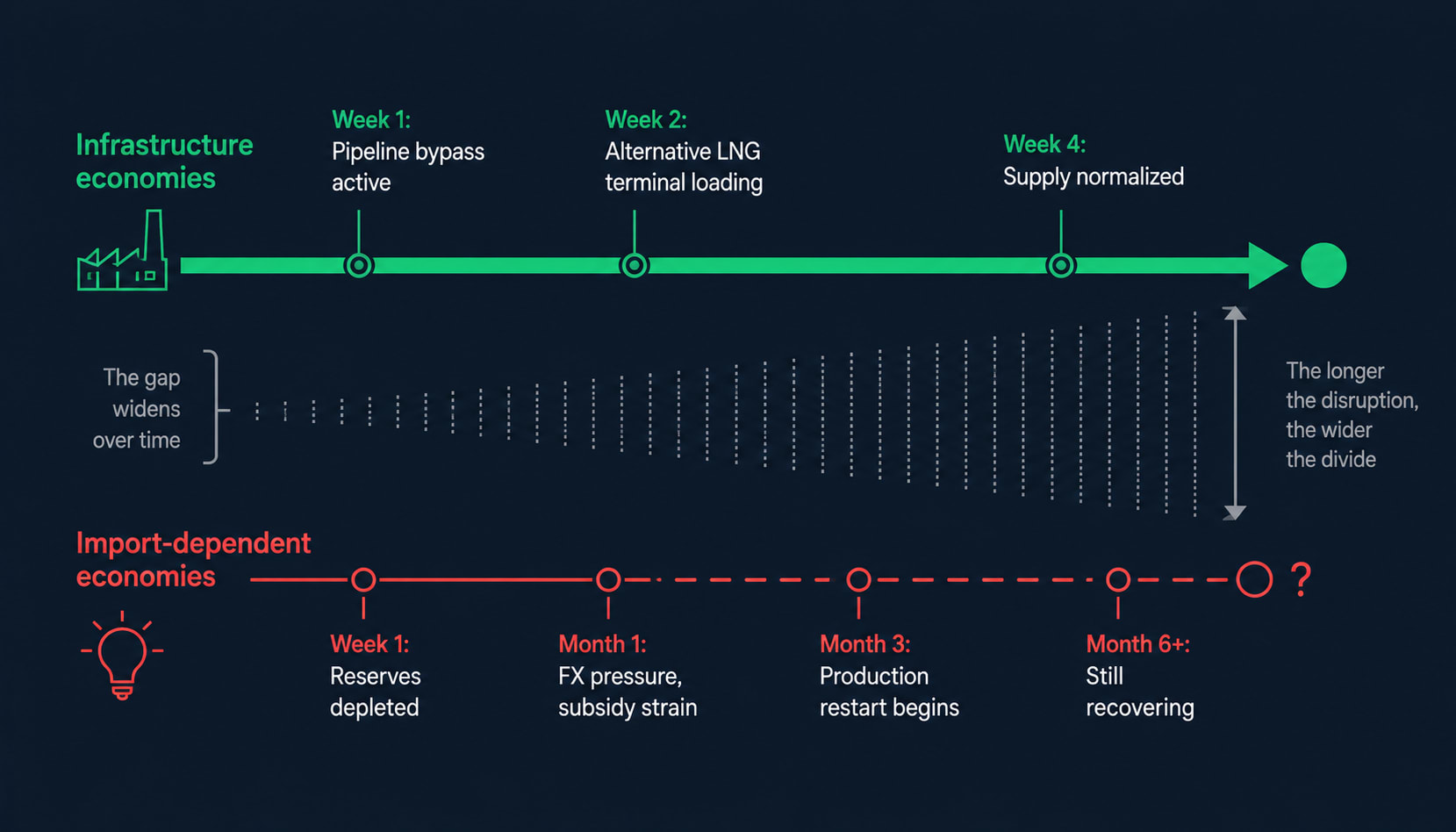

§3 — Two Speeds of Recovery

The third structural exposure is the recovery asymmetry — the fact that the same supply disruption produces radically different outcomes depending on who is receiving the supply.

Economies with pipeline infrastructure, diversified import routes, or domestic production capacity responded to the Hormuz closure through substitution. European importers activated pipeline alternatives. US domestic refiners drew on Permian Basin production. Gulf Cooperation Council members with refinery capacity processed local crude directly. For these economies, the closure was an expensive inconvenience. Normalisation happened in weeks.

Import-dependent economies without alternatives faced a different arithmetic. With five to twenty-three days of reserve cover and no viable substitute supply route, the closure was not an inconvenience. It was an emergency that reserve systems were designed to manage over days — not a crisis that persisted for more than one hundred days, closing three times.

The recovery asymmetry is not primarily a function of wealth. Japan, a wealthy economy, holds 254 days of cover. Pakistan holds five. But the divergence is also not primarily a function of income. It is a function of prior infrastructure investment — the deliberate choice, made over decades, to build or not build the storage and supply network that converts a temporary disruption into a manageable event.

Hormuz did not create the two-speed recovery. It made the underlying infrastructure gap visible under stress conditions that had not existed before.

§4 — What Ships Must Carry Now

The International Maritime Organization reported that more than 2,000 vessels and 20,000 seafarers were stranded in the Persian Gulf at the peak of the crisis. Not all were trapped in the same way — some regional operators continued local routes, some vessels eventually transited via Iranian-controlled corridors — but the physical consequences of prolonged anchorage applied across the fleet.

Vessels anchored for weeks rather than days accumulate maintenance arrears that do not reverse when the anchorage ends. Underwater hull growth that would normally be addressed at scheduled drydock intervals accelerates in warm, shallow Gulf waters. Machinery systems designed for operational cycles rather than extended idle periods require inspection or repair before returning to full service. Crew certification windows that assume continuous employment run against hard ITF and MLC compliance deadlines that anchorage does not pause.

Of the stranded fleet, Kpler identified 118 laden tankers — fully loaded with crude, unable to deliver, their hire accruing against cargo that could not move. When those vessels eventually exit, the one-time surge will temporarily inflate the available fleet before normalising — a pattern visible in every prior supply restoration where stranded tonnage re-enters a market that has spent months adjusting to its absence.

The physical degradation from the 2026 Hormuz anchorage will not appear in freight rate data. It will appear in drydock schedules in Q3 and Q4, in fleet availability figures that diverge from nominal capacity, and in the gap between what the orderbook predicts and what the effective fleet delivers. This is the cost that does not show up in the oil price. The barrel is priced when it is loaded. The cost of the ship that carries it — maintained, certified, crewed, and available — is priced separately, through a market that the oil trade depends on but does not fully control.

§5 — Oil Is Still the Operating System

Three times in one hundred days the Strait of Hormuz closed. Three times the coordinated response of the IEA, the SPR releases, the diplomatic channels, the rerouting alternatives, and the reserve cover held — partially, unevenly, at enormous cost. The crisis produced the largest reserve release in IEA history, the highest VLCC freight rates ever recorded, and a recovery asymmetry between infrastructure economies and import-dependent ones that will take years to close.

None of this happened because of a failure of markets, or of logistics, or of political coordination. It happened because oil is still the operating system of the global economy, and that operating system runs through a single chokepoint that has no bypass, no redundancy, and no alternative.

The transitions that are supposed to be replacing oil — renewable electricity, battery storage, green hydrogen — are real. They are also slow. In 2025, oil supplied roughly 31% of global primary energy. Natural gas, much of which transits Hormuz as LNG, supplied another 24%. The combined share of energy sourced from molecules that move on ships through chokepoints exceeds 50% of global primary energy consumption. That share declines every year. It did not decline enough before February 2026 to make the Hormuz closure a manageable disruption.

The lesson of the crisis is not that Hormuz is fragile. It has always been fragile. The lesson is that the system built on top of it — the refinery, the power plant, the data centre, the reserve stockpile, the laden tanker, the seafarer on anchor watch — cannot be rerouted, patched, or arbitraged away. It can only be sailed through.

That is why ships matter. Not as a sector, not as an asset class, not as a supply chain input. As the operating layer of a global energy system that is, for now, still made of molecules that move on water.

- International Energy Agency, Emergency Oil Stock Release decision and member country reserves data (March 2026)

- U.S. Energy Information Administration, Strategic Oil Inventories assessment (April 2026)

- Spark Commodities, Spark30S and Spark25S LNG spot freight assessments via LNG Prime (June 2026)