A 180,000-deadweight-tonne Capesize bulk carrier costs around $70 million to build. The same ship, in 2026, can earn its owner roughly $3 million on a single Atlantic voyage carrying iron ore from Brazil to China. Or it can earn the owner around $50 million over five years on a long-term charter to a steel mill. Or it can earn a steady, predictable hire of around $10 million a year for fifteen years — roughly $150 million across the full term — on a financing arrangement where someone else operates it entirely.

Same ship. Same crew, in the first two cases. Three completely different commercial outcomes, decided at the moment the charter contract is signed.

The document that decides which of these outcomes happens — which costs the owner pays, which the charterer pays, who loses when bunkers spike, who wins when freight rates fall — is called the charter party. The name is centuries old. The underlying framework was settled, in its modern form, more than a hundred years ago. And almost every fixture in the commercial shipping world today still starts from one of a handful of standard documents that have been in continuous use since well before any of the ships were built.

It is worth understanding what each one actually does. Let's walk through it the way a chartering desk reads it.

What a charter party actually is

A charter party is a contract for the hire of a ship. It sets out the terms under which the shipowner makes the vessel available, what the charterer is allowed to do with it, how the payments work, who pays for which costs, and what happens when something goes wrong.

The name has nothing to do with parties in the political or celebratory sense. It comes from the medieval Latin carta partita, meaning "divided document." The original practice was elegant in its simplicity: the contract was written twice on a single sheet of paper, the sheet was then cut in half along a deliberately irregular line, and each party kept one half. To verify the agreement later, the two halves had to be fitted back together — the matching torn edges served as proof of authenticity. No signatures, no seals, no notary. The geometry of the cut was the verification.

The same logic gave English law a related word: indenture. An indenture was a contract cut along a jagged or "toothed" edge — the teeth of the two parts had to refit to confirm the document was genuine. Charter party and indenture are linguistic cousins, both born from the same medieval verification technology. The physical cutting of paper has long since stopped. Both names stayed.

Charter parties have been a structural element of maritime commerce for centuries, but the standardised forms used today mostly trace their lineage to the early twentieth century. The Baltic and International Maritime Council, known as BIMCO, is the dominant publisher. BIMCO was founded in 1905. BIMCO marked its 120th anniversary in 2025. Today it has approximately 2,100 member companies in around 120 countries, representing about 64% of the world's merchant tonnage. Its membership covers shipowners, operators, managers, brokers, and agents — essentially every commercial party that hires or operates ships. Its standard forms, refined and re-issued over many decades, are what almost every commercial fixture in the world starts from.

The three primary types of charter party — voyage, time, and bareboat — answer the same question in three different ways: how much of the operational responsibility transfers from the shipowner to the charterer when the ship is hired? The question matters because every line of cost the charter party shifts is a line of cost the other party no longer pays.

Three ways to hire a ship

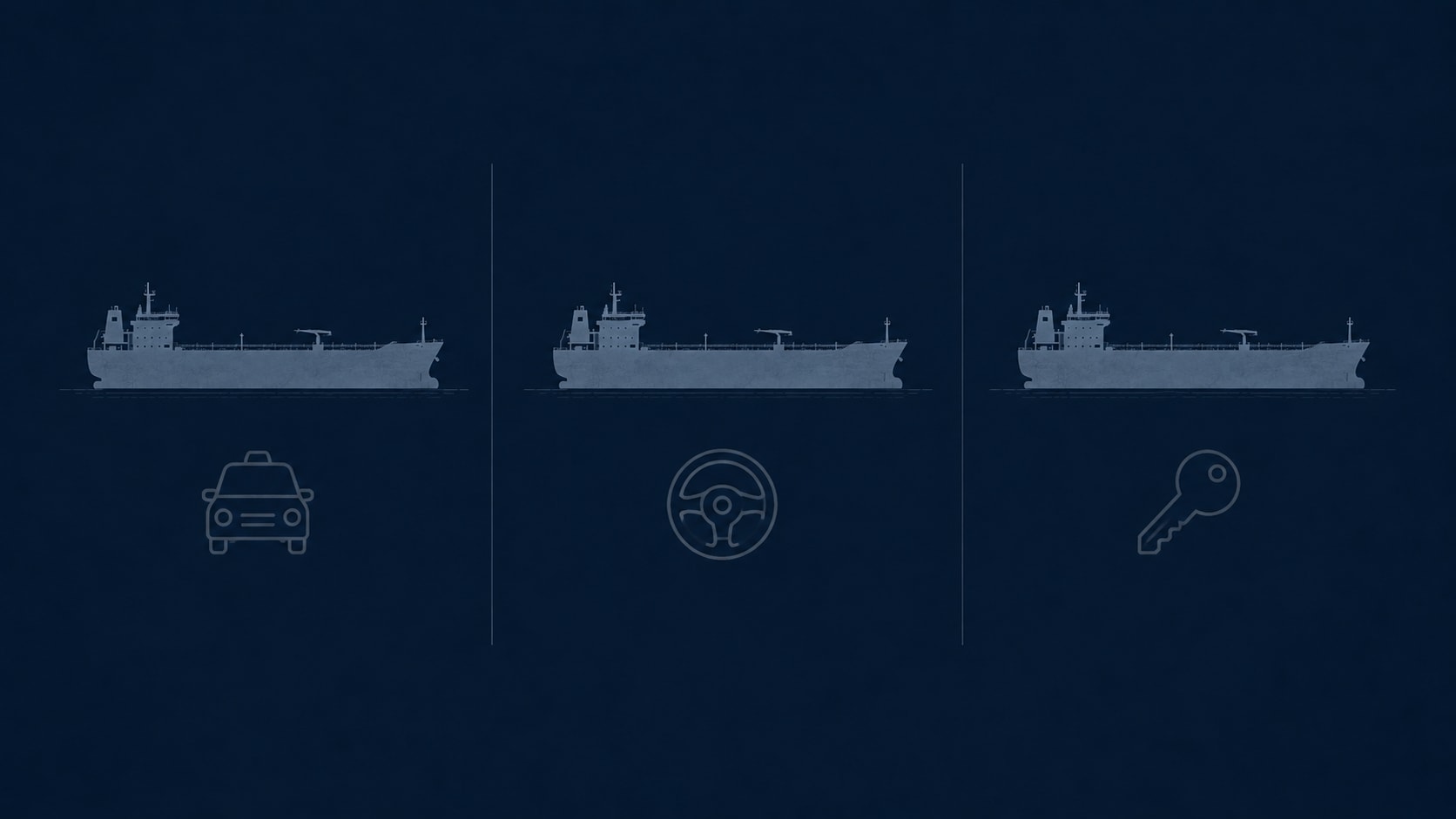

The easiest way to understand the three charter types is by analogy to renting a car.

Voyage charter — like booking a taxi. You tell the driver where you want to go. You pay the agreed fare. The driver handles everything else — the route, the fuel, the parking fees at either end. If traffic is bad and the trip takes longer, that is the driver's problem. You just pay the fare and get out at the destination.

In a voyage charter, the shipowner agrees to carry a specified cargo from a load port to a discharge port for an agreed freight rate — usually expressed in dollars per tonne of cargo carried, or sometimes as a lump sum. The owner is responsible for nearly all the costs of the voyage: bunker fuel, port charges, canal dues, crew wages, maintenance, hull insurance. The charterer's job is to provide the cargo and pay the freight.

Time charter — like renting a car with a driver. You hire the vehicle and its driver for a defined period — a day, a week, a month. You decide where it goes. You pay for the petrol, the parking, the tolls. The owner of the car still employs the driver and keeps the car maintained. You direct; the owner provides.

In a time charter, the shipowner provides the vessel and the crew. The charterer takes commercial control: where the ship goes, what it carries, how fast it steams. The charterer pays a daily hire rate, plus all the variable voyage costs — bunker fuel, port charges, canal dues. The owner still pays the crew wages, the maintenance, the hull insurance. The hire is paid in advance, usually every fifteen or thirty days, for the duration of the charter.

Bareboat charter — like leasing a car with no driver. You take the car. You take the keys. You hire your own driver, you pay for the petrol, the maintenance, the insurance. The only thing the leasing company still owns is the vehicle itself. You operate it as if it were yours, for the duration of the lease.

In a bareboat charter — also called a demise charter — the charterer takes legal and operational possession of the ship. The charterer hires the crew, arranges insurance, pays for maintenance, pays for fuel, pays for everything. The owner retains title to the vessel but transfers essentially every other responsibility. Bareboat charters typically run for years rather than months, and very often function as a form of ship financing: the bareboat charterer is, in effect, the real economic operator, with a purchase option at the end of the contract.

That is the headline structure. The detail is where the money sits — and that detail decides millions of dollars per fixture.

Who pays for what

The single most important question in any charter party is the allocation of costs. Every cost the contract assigns to the shipowner is a cost the charterer does not pay, and vice versa. A handful of cost categories matter most: crew wages and provisions, bunker fuel, port charges, canal dues, cargo loading and discharge, vessel maintenance, hull and machinery insurance, protection and indemnity (P&I) cover, and the capital cost of the ship itself.

The pattern matters because it determines who carries which market risks. A voyage-charter owner carries the bunker price risk for the duration of the voyage. A time-charter owner does not — the charterer pays for bunkers and absorbs that volatility. A bareboat owner carries no operational market risk at all; the charterer absorbs everything.

When bunker prices spike, voyage-charter owners get squeezed on already-fixed freight rates while time-charter owners continue to collect hire as if nothing has changed. When freight rates collapse, time-charter owners keep collecting hire on fixed-period charters while voyage-charter owners watch their spot earnings disappear. The choice of charter type is, in part, a choice about which kind of risk an owner wants to carry.

The standard forms

Almost nobody negotiates a charter party from a blank page. The standard forms published by BIMCO and a small number of industry associations are the starting point for nearly every fixture in the world. Each form has a name and a year, and the year tells you something about the industry's history.

The oldest still in regular use is BALTIME, a time charter form for dry cargo first issued in 1909. The current version is BALTIME 1939 (revised 2001). The name reflects the form's origin in the Baltic Exchange in London, which was already the centre of global dry bulk chartering when the document was first drafted.

GENCON is the world's most widely used voyage charter form for dry bulk. It was first developed in 1922 and revised in 1976 and 1994. The current edition, GENCON 2022, was published on 25 October 2022 — exactly one hundred years after the first edition, and the first revision since 1994. The new version roughly doubles the length of its predecessor and was designed to handle the sanctions exposure, war-risk clauses, and environmental requirements that the 1994 form was never written for.

NYPE — the New York Produce Exchange form, first issued in 1913 — is the most widely used time charter form in dry cargo. The current version is NYPE 2015, dated 3 June 2015, the product of three years of joint drafting between BIMCO, the Association of Ship Brokers and Agents (ASBA, the form's copyright holder), and the Singapore Maritime Foundation. The form runs to 57 clauses and 32 pages, roughly twice the length of NYPE 1993. The previous version, NYPE 93, is still in circulation on older fixtures.

SHELLTIME is the equivalent time charter form for tankers, published by Shell. ASBATANKVOY is a widely used standard voyage charter form for tankers. BARECON is the BIMCO standard for bareboat charters. It was first published in 1974 as two separate forms (BARECON A and B), amalgamated into a single document in 1989, and revised in 2001 and again in 2017. The current version is BARECON 2017.

Each of these forms is, in effect, a starting kit. A typical fixture begins with the standard form and then adds rider clauses — bespoke provisions that adjust the standard text for the specific cargo, ports, sanctions exposure, payment terms, environmental requirements, and commercial balance the two parties have agreed. A real charter party can run to forty or fifty pages once the riders are attached.

The fact that the underlying forms have remained in continuous use across a hundred years — through two world wars, multiple oil crises, the containerisation of liner trade, the rise and fall of major flag states, and the IMO's 2020 sulfur cap — tells you something useful. The commercial structure of how ships get hired is one of the most stable things in shipping. Markets change. The forms absorb the change in their riders and revisions.

Laytime, demurrage, and despatch

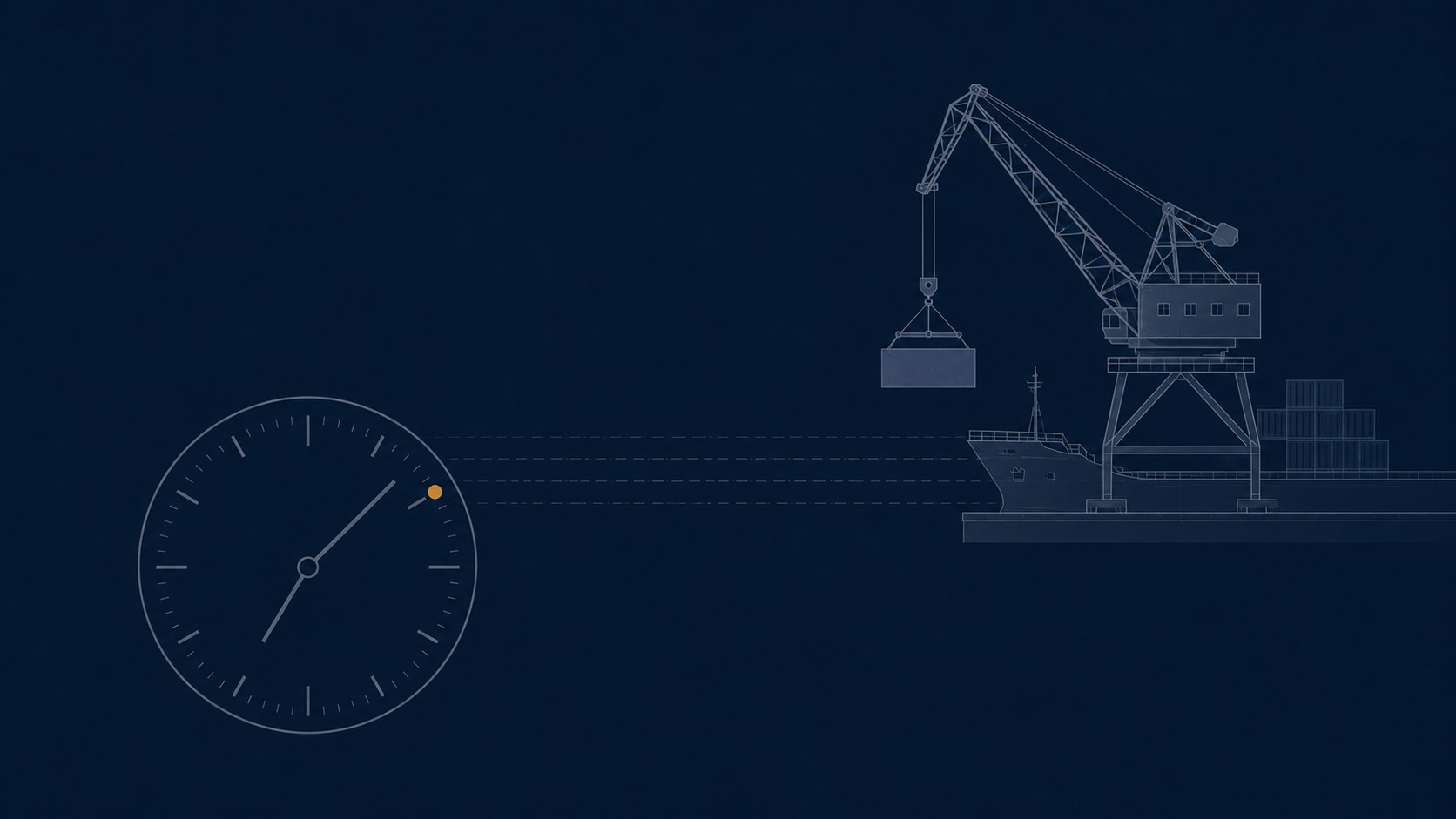

A voyage charter has a clock built into it. That clock is called laytime, and the rules around it are some of the most heavily negotiated terms in the contract.

Laytime is the period the charterer is allowed for loading and discharging the cargo. It is fixed in the charter party — for example, 36 hours total for loading plus discharging, or three days at each end, or a calculation based on a daily handling rate ("3,000 tonnes per weather working day"). The clock does not start automatically when the ship arrives. It starts when the master tenders a Notice of Readiness (NOR) — a formal declaration that the vessel has arrived, is in all respects ready to load or discharge, and the laytime clock is now running.

If the charterer finishes within laytime, no extra payment is due. If the charterer goes over, demurrage applies. Demurrage is a daily rate, agreed at the time of the fixture, that the charterer pays the owner for every day (or part of a day) beyond laytime. It is compensation for the fact that the ship is sitting at a port, earning no other revenue, because the charterer has not finished loading or discharging.

These numbers compound. A VLCC held three days over laytime at a congested discharge port can produce a six-figure demurrage claim from a single fixture. In stressed markets — the 2026 Hormuz disruption being a recent example — actual demurrage claims on VLCC fixtures have pushed well past the normal-market range. Charterers structure their port operations specifically to avoid them.

If the charterer finishes early, the owner usually pays despatch — a kind of opposite-of-demurrage, where the shipowner compensates the charterer for the time saved. Despatch is typically set at half the demurrage rate (the shorthand is "despatch half demurrage," or DHD). One important quirk: despatch is conventional in dry bulk chartering but is essentially absent in tanker chartering. A tanker charterer who finishes ahead of laytime gets no financial benefit; a bulker charterer in the same position gets paid for the time saved.

Time charters do not have laytime or demurrage in the same form, because the charterer pays continuously for the whole charter period anyway. They do have an analogous concept called off-hire — periods when the vessel is unavailable for the charterer's use (breakdown, drydocking, certain crew issues) and during which the hire payment is suspended. The language of off-hire is one of the most negotiated areas in time charter fixtures, because every clause defines whether the owner loses revenue when the ship cannot trade. Bareboat charters have neither demurrage nor off-hire in the traditional sense. The charterer pays hire for the full duration of the contract regardless of how the ship is performing, because the charterer is, for all operational purposes, the operator.

Why bareboat is often a financing structure

The first two charter types — voyage and time — are straightforwardly about hiring a ship to do commercial work. Bareboat is often something different.

A typical bareboat charter runs for ten years, fifteen years, or longer. The charterer takes the ship, hires the crew, operates it commercially, pays a fixed monthly hire to the owner, and at the end of the term, frequently has the option to purchase the vessel outright. The structure looks less like a rental and more like a long-term lease with a built-in purchase option.

This is not accidental. Bareboat charters are widely used as ship-financing arrangements. A company that wants to operate ships but does not want the full balance-sheet weight of owning them can arrange a sale-and-leaseback structure: build the ship, sell it to a financing institution, and then charter it back on a bareboat basis. The financing institution becomes the legal owner. The operating company remains the commercial operator. Cash flows match an operating expense rather than a capital expense.

Bareboat charters also enable flag-of-convenience arrangements. A vessel registered in one jurisdiction can be bareboat-chartered to an operator who registers the vessel under a different flag for the duration of the charter (known as a bareboat registry). The owner stays in the first jurisdiction. The operating flag changes. This structure is common, legal in most jurisdictions, and a recurring source of regulatory attention.

The result is that the bareboat charter, despite being the oldest and most extreme form of ship hire, is in 2026 often not really a "charter" in the commercial sense at all. It is a financing instrument that uses the legal architecture of a charter party to achieve a balance-sheet outcome. Reading a bareboat fixture and looking only at the daily hire rate misses what the contract is actually doing.

Reading the market

For anyone trying to follow commercial shipping without sitting on a chartering desk, the choice of charter type is one of the most informative pieces of market information publicly available.

When voyage-charter activity is rising, it usually means charterers expect freight markets to fall. They want to lock in specific cargo movements at current rates without committing to extended periods of vessel hire.

When time-charter activity is rising — particularly long-period time charters of one, three, or five years — charterers are usually expecting markets to rise. They want to lock in current rates for an extended period before they go higher.

When bareboat activity is rising, something else is usually happening: ship-financing transactions, fleet restructurings, flag-state arbitrage, or strategic positioning by major operators. Bareboat volumes correlate less with current freight markets and more with capital availability, regulatory shifts, and longer-term industrial strategy.

The same ship, in the same market, can be voyage-chartered at WS 280 to lock in spot earnings during a tanker spike, time-chartered at $40,000 a day to capture an expected six-month tightness, or bareboat-chartered at $15,000 a day for fifteen years to a financing counterparty. Three quotes, three different answers about what the owner thinks happens next.

The charter party is the contract. The choice of which one is the read.

For more on the commercial systems that sit alongside the charter party, see our companion pieces on What Is Worldscale?, What the Baltic Dry Index Tells You, Tanker Sizes Explained, and Classification Societies Explained.