In January 2025, the gas carrier Clipper Eris left a Singapore drydock with a 7-megawatt carbon capture system bolted onto its exhaust line. Over the following twelve months, the system pulled up to 70 percent of the CO2 out of the ship's engine exhaust, liquefied it, and stored it in deck tanks. Wärtsilä's commercial launch in May 2025 followed earlier CCS-ready scrubber orders, including a September 2024 contract with German operator Leonhardt & Blumberg for three containerships.

This is what onboard carbon capture looks like now. Not a concept. A working ship. Commercial voyages. Verifiable tonnes of CO2 separated from exhaust streams. Around fifteen vessels were running OCCS systems by end-2025, according to Bureau Veritas estimates. Three years earlier, deployments were limited to single-digit pilots.

The shipping industry has been debating alternative fuels for half a decade. Methanol orderbooks have stalled. Ammonia is years from scale. Hydrogen remains marginal. Meanwhile, a different decarbonization path quietly crossed from research to deployment.

The technology works. The question is what it costs, and what happens to the CO2 once the ship reaches port.

What OCCS Actually Is

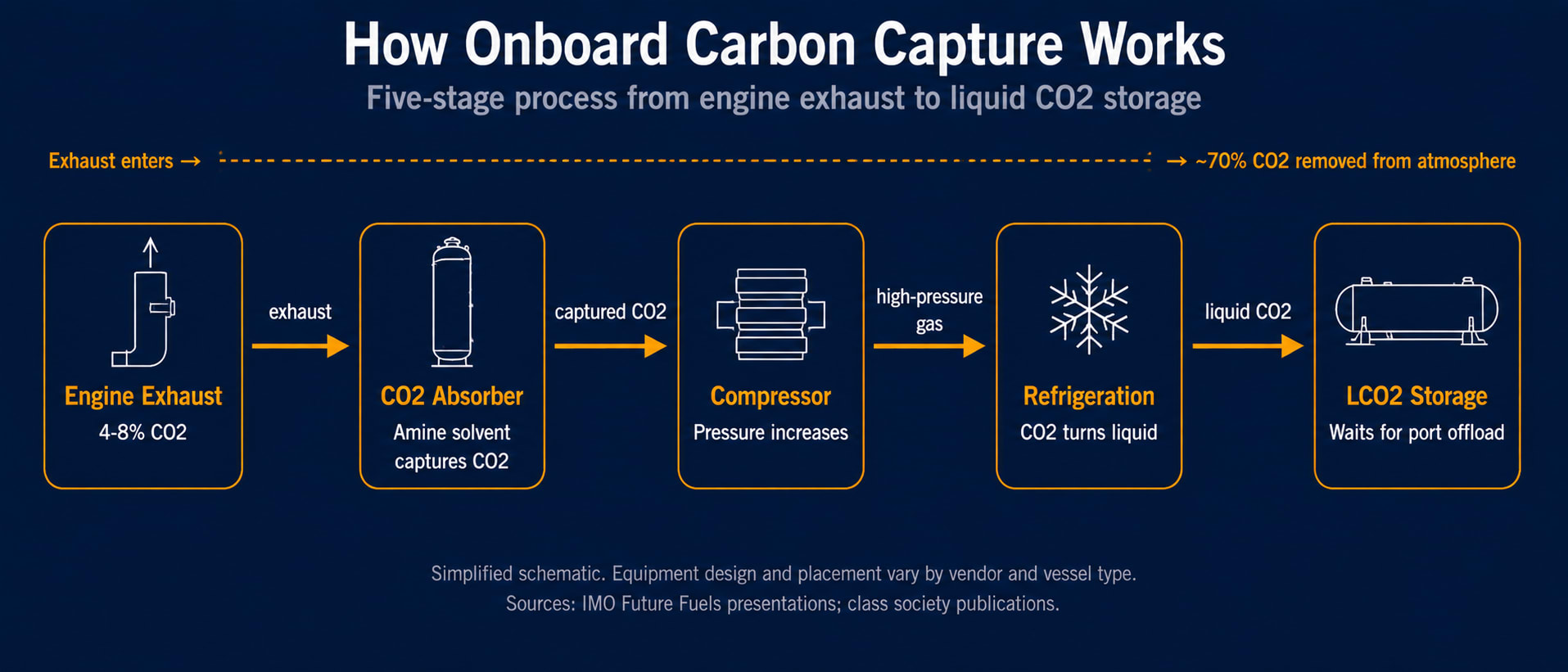

OCCS is not a brand. It is a category of equipment. Systems bolt onto a ship's exhaust line, extract CO2 from the flue gas before it leaves the funnel, liquefy it through compression and refrigeration, and store it in deck tanks until the vessel reaches a port that can receive it.

The chemistry is mature. Most current systems use amine solvents — liquid chemicals that absorb CO2 from the exhaust stream at 4–8 percent concentration, then release it under heat or pressure for compression. The dilute exhaust is why OCCS is energy-intensive: the system has to concentrate CO2 from a low base, which costs roughly 10 percent in additional fuel consumption.

Variants exist. Carbon Ridge, a US developer, deployed a centrifugal system on the Scorpio Tankers LR2 product tanker STI SPIGA in July 2025, with a smaller footprint than conventional absorption columns. Seabound, a UK startup, deployed a commercial calcium-looping system on a Heidelberg Materials cement carrier in mid-2025, converting captured CO2 into calcium carbonate — eliminating the need to keep carbon in liquid form.

Capture rates are real but bounded. Most full-scale systems target 50 to 80 percent of engine exhaust CO2, with the higher end achievable only in specific conditions. The annualized net reduction is lower than the peak. Project REMARCCABLE, a joint study by Stena Bulk and partners on the MR tanker Stena Impero, estimated a 19.7 percent annual net CO2 reduction at a 9.2 percent fuel penalty.

That fuel penalty is the first economic constraint. The system reduces emissions but increases consumption. Whether the trade is profitable depends on the carbon price the ship would otherwise pay.

Why Gas Carriers Went First

The first commercial OCCS deployments were not random. Clipper Eris is a gas carrier. Stena Impero is a product tanker. STI SPIGA is a tanker. Nexus Victoria, MOL's installation with Value Maritime's Filtree system, is also a product tanker.

The pattern is not coincidence. Three structural reasons drove tankers and gas carriers into the first wave.

Deck space. LCO2 storage tanks are large — the two tanks on Clipper Eris measure roughly 28 metres long and 4 metres in diameter each, sitting on the deck near the funnel. Container ships have limited free deck space between cargo bays. Bulk carriers have hatches across most of the deck. Tankers and gas carriers have open deck areas where storage tanks can be installed during a retrofit without sacrificing cargo capacity.

Liquefaction familiarity. Gas carriers already operate cryogenic equipment for their primary cargo. The crew, the engineering systems, and the operating procedures for handling pressurized liquefied gas are already in place. Adding LCO2 storage to a gas carrier is an extension of existing operations. Adding it to a container ship is a new operating capability.

CII pressure. Tanker and gas carrier operators face carbon intensity indicator targets under IMO rules. A capture system that reduces operational CO2 by 15–20 percent translates directly into improved CII ratings. For container lines on EU trades, the same arithmetic applies under EU ETS — but the deck constraints make retrofit harder.

The early adopter pattern is therefore engineering-led, not marketing-led. The vessels that can fit OCCS, run it, and book the compliance credit moved first. Container shipping is following, but slower.

The Ten-Times Cost Gap

This is where the OCCS story splits into two narratives, and the gap between them defines the next three years.

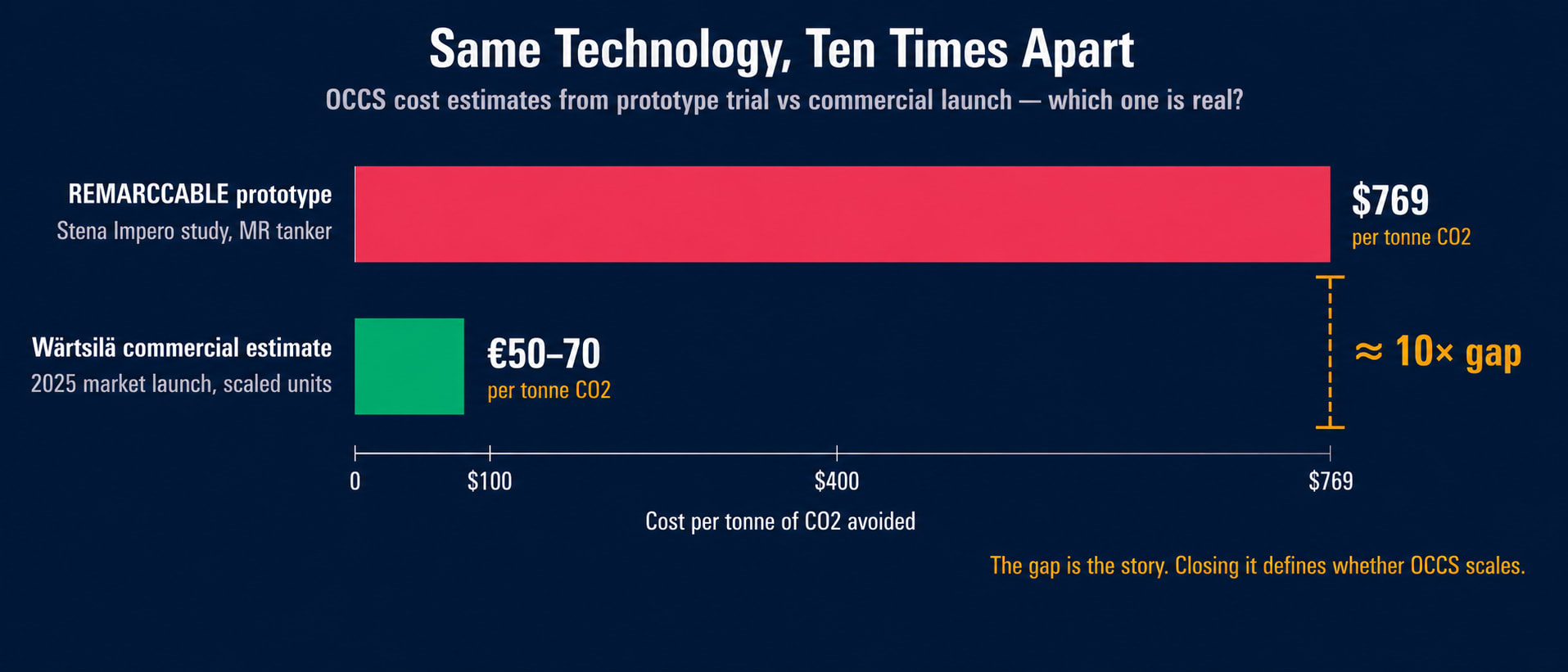

Project REMARCCABLE published a prototype cost estimate in 2024: roughly $769 per tonne of CO2 avoided, based on a $13.6 million system installation on the Stena Impero. The number was widely cited as evidence that OCCS was too expensive to scale.

Wärtsilä launched its commercial product in May 2025 with a published cost estimate of €50–70 per tonne CO2 avoided, including capital and operating costs over the system lifetime. That is roughly $54–76 per tonne at current exchange rates — comparable to current EU ETS allowance prices.

The two numbers are not contradictory. They measure different things. The REMARCCABLE figure reflects a single prototype installation with high one-off engineering costs and conservative assumptions. The Wärtsilä figure reflects scaled production, optimized engineering, and amortization across multiple installations. But the spread between them — roughly ten times — is also not yet resolved by independent third-party verification.

If Two Clocks of Shipping framed the gap between freight indices, OCCS shows another gap on a slower clock — between prototype economics and commercial economics, with no transparent path to confirming which one is real.

For shipowners evaluating OCCS, this is not an academic question. The difference between $769 and €70 per tonne is the difference between an uneconomic compliance cost and a competitive alternative to ammonia or methanol. The commercial estimate, if it holds at scale, makes OCCS viable on EU trades today. The prototype estimate, if it holds, makes OCCS a niche solution.

The market has not yet decided which estimate to trust. Neither has the IMO. The next two years of commercial deployments will produce the data that resolves the gap — or widens it.

The Port Problem

This is where the technology stops being the constraint.

A vessel running an OCCS system captures CO2, liquefies it, and stores it on deck. The ship reaches port. The CO2 needs to come off. From there, it needs to be transported to either a sequestration site (permanent underground storage) or a utilization facility (industrial reuse, food-grade applications, e-fuels production).

That value chain almost does not exist for ship-captured CO2.

A 2024 study commissioned by the Global Centre for Maritime Decarbonisation, with Lloyd's Register and ARUP, examined port readiness for receiving liquefied CO2 from ships. The findings were direct. The technologies for offloading exist at high maturity levels — these are the same valves, hoses, and storage tanks used for liquefied gas handling for decades. What does not exist is operational integration. Trained personnel for safe CO2 transfer at scale have not been demonstrated. The limited number of ports with any LCO2 infrastructure are designed for food-grade CO2, not the volumes ship-captured CO2 would represent.

The study identified over ten LCO2 infrastructure projects worldwide in some phase of planning. Most are still in concept phase. None have reached Final Investment Decision. The reason is straightforward: ports will not invest in offloading infrastructure until enough ships carry CO2 to make it pay. Shipowners will not invest in OCCS at scale until ports can receive the CO2. The chicken-and-egg dilemma, played out on asset cycles measured in decades.

Anyone who has watched LCO2 handling at an industrial terminal understands what is missing. The valves exist. The hoses exist. What does not exist is the muscle memory — the trained crews, the buffer zone planning, the documentation standards, the cross-border accounting rules. None of it is technically hard. All of it is institutionally slow.

The operator's nightmare is real. A vessel reaches a major port with 700 cubic metres of LCO2 in deck tanks. No terminal has the contract, the personnel, or the storage to receive it. The ship cannot discharge. The next loading port also lacks the infrastructure. The captured CO2 becomes a logistical liability instead of a compliance asset.

This is the scenario shipowners are quietly modeling.

The Regulatory Arbitrage

The EU Emissions Trading System reached 100 percent compliance coverage for shipping in 2026 — meaning every tonne of CO2 emitted on EU-touching voyages now carries a direct monetary cost. At the May 2026 EU ETS average price of around €74 per tonne, a Suezmax tanker emitting roughly 30,000 tonnes of CO2 per year on EU routes carries an annual compliance cost of approximately €2.2 million.

The EU ETS framework is being updated to address CCS and CCU, with preliminary guidance in place. Captured CO2 that is permanently sequestered or fixed in qualifying products (such as construction materials) can reduce surrender obligations. FuelEU Maritime does not yet recognize OCCS, creating policy inconsistency. The treatment of operationally captured shipboard CO2 — temporarily stored, transported, then sequestered or utilized — is still being clarified through guidance and implementing acts.

The IMO does not yet have a settled position either. A Correspondence Group was established at MEPC 83 in April 2025 to develop the OCCS regulatory framework. The work plan is targeted for completion in 2028. Until that framework lands, captured CO2 has no clear status in the IMO Net-Zero Framework — it cannot reliably be claimed against IMO fuel intensity targets.

This is the regulatory arbitrage. A ship trading exclusively into EU ports today can monetize OCCS through EU ETS — partially, and subject to evolving rules. A ship trading globally cannot — at least not until 2028, when the IMO framework finalizes.

The implication for fleet deployment is direct. Vessels on EU–Asia container trades, EU-touching tanker routes, and Northern European short-sea operations have an asymmetric incentive to install OCCS now. Vessels on Pacific or trans-Atlantic non-EU routes do not. The first wave of commercial deployments reflects this — the Clipper Eris voyage schedule, the Pacific Cobalt routing, the Ever Top trade lane all include EU port calls.

The geographic concentration is not the technology's preference. It is the regulatory map.

What to Watch in 2026–2028

Three signals will determine whether OCCS scales or stalls.

First, the IMO framework. NZF adoption itself is scheduled for the resumed MEPC/ES.2 in October 2026, with earliest entry into force March 2028. MEPC 85 in late 2026 should advance OCCS-specific testing, survey, and certification guidelines. If that sequence holds and OCCS is treated comparably to alternative fuels in IMO accounting, the technology becomes a viable compliance path for non-EU trades. If the timeline slips, OCCS remains a regional EU solution.

Second, port Final Investment Decisions. The first major port to commit to commercial-scale LCO2 offloading infrastructure — likely Rotterdam, Singapore, or a Norwegian hub — will trigger a sequencing effect. Once one major port has operational capacity, shipowners on related trade routes can plan voyage cycles around offloading. The current freeze in port investment will lift only when the regulatory framework and minimum vessel fleet make the case for FID.

Third, the cost convergence. The next eighteen months of Wärtsilä, Carbon Ridge, Seabound, and Value Maritime deployments will produce real production cost data. If commercial costs settle near €50–70 per tonne, OCCS becomes economically competitive on most EU trades. If they drift toward the prototype $769 figure, OCCS remains niche. If they fall below €50 with scale, OCCS reshapes the alternative fuels conversation.

The market is currently pricing OCCS as if the prototype number is real. The vendors are pricing as if the commercial number is real. One side is wrong.

Implications

For shipowners with significant EU exposure, OCCS has entered serious capital-planning conversations. Vessels coming through major refit cycles in 2026–2028 — particularly LPG carriers, LNG carriers, and product tankers on European trades — should evaluate OCCS retrofit feasibility against ammonia-ready newbuild costs. The first-mover position is increasingly defensible.

For ports and port authorities, the chicken-and-egg dilemma is itself the strategic question. The first port to make the capital commitment will capture the early OCCS fleet. The cost of waiting is lower than the cost of building too soon — but waiting also concedes positioning to competitors. Singapore, Rotterdam, and the Norwegian hub authorities are all in early-stage planning. The race is not yet visible. It will be.

For charterers and cargo owners with ESG mandates, OCCS-equipped vessels are beginning to differentiate at the contract level. Premium freight rates for verifiable carbon-managed voyages are emerging in specific corridors. The voluntary carbon market and corporate scope-3 accounting are converging on shipping in ways that did not exist two years ago.

Closing

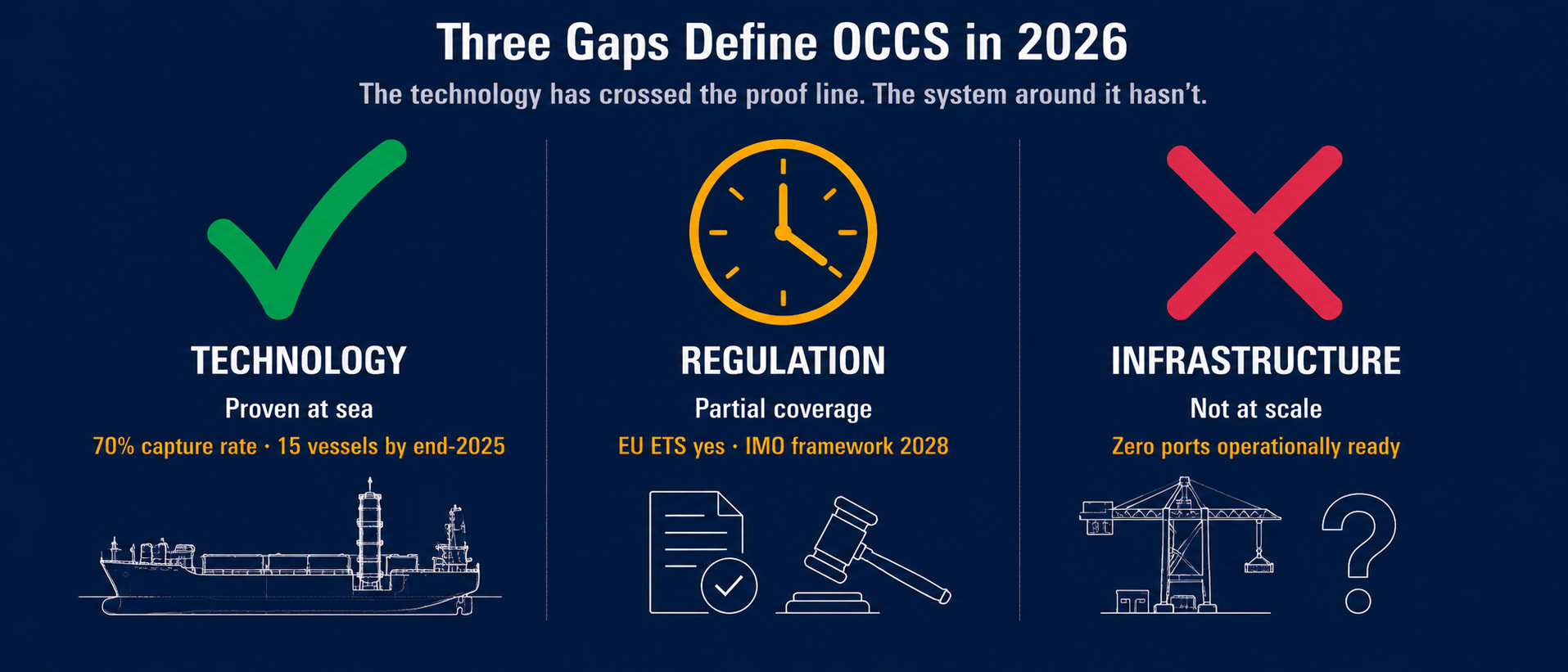

OCCS is the rare maritime technology that has crossed the proof-of-concept line without solving the deployment problem. The chemistry works. The engineering works. Capture rates are verified, abatement is measurable, systems are operating on commercial vessels right now.

What is missing is everything outside the ship. Port infrastructure. Regulatory framework. Cost convergence. CO2 disposition pathways. Each gap can be closed. None has been closed yet.

In the broader decarbonization debate, the alternative fuels story dominates attention. Ammonia and methanol and hydrogen each have their own bottlenecks, their own infrastructure problems, their own decade-long deployment runways. The Quiet Retreat of alt-fuel orderbooks in late 2025 made that clear. OCCS sits alongside that debate, quietly proving that capture-and-store can be a parallel path — neither replacing alternative fuels nor competing with them, but extending the useful life of conventional fuels by stripping carbon at the source.

The technology works. The infrastructure doesn't. The cost gap is unresolved. Whoever closes those three gaps first — port, regulator, or commercial operator — will set the price of carbon at sea for the next decade.