A bunker procurement contract signed in early 2024 covered four emission control areas: the Baltic Sea, the North Sea, the North American ECA, and the U.S. Caribbean Sea. A bunker procurement contract signed in early 2028 will cover eight. Three of the four new zones are in waters that handle some of the world's heaviest tanker, container, and bulker traffic. The fourth is in the Canadian Arctic, where shipping volume is small today but growing as polar routes open.

This is the largest regional restructuring of the marine bunker market since IMO 2020 took effect six years ago. It is happening in three steps:

- May 1, 2025 — Mediterranean Sea becomes the fifth ECA (SOx and particulate matter)

- March 1, 2026 — Canadian Arctic and Norwegian Sea ECAs enter force (SOx, PM, NOx); 12-month grace period before the 0.10% sulfur limit applies on March 1, 2027

- September 1, 2027 — North-East Atlantic Ocean ECA enters force (SOx, PM, NOx); 0.10% sulfur limit applies September 1, 2028

By the second half of 2028, almost every commercial route between northern Europe, the Mediterranean, the North Atlantic basin, and North America will pass through at least one 0.10% sulfur zone. Most major routes will pass through several. The bunker market is rebuilding around the new map.

The Mediterranean ECA, the only one of the new zones that has been operating long enough to produce hard data, shows what happens when a zone goes live. Year one was sharper than the industry expected.

The Mediterranean, the Arctic, and the Atlantic

The ECA expansion is not one event. It is three separate regulatory steps spread across three years, each redrawing a different commercial geography.

The Mediterranean took effect on May 1, 2025. The Canadian Arctic and Norwegian Sea ECAs entered force on March 1, 2026, with sulfur restrictions following on March 1, 2027. The North-East Atlantic ECA enters force September 1, 2027, with sulfur restrictions on September 1, 2028. By the second half of 2028, all three transitions are complete and the cumulative geography is in place.

Each step applies the same contractual rule — fuel sulfur capped at 0.10%, NOx Tier III for new ships, particulate matter controls. The difference is which trade absorbs the rule and when. The Mediterranean encloses a basin that, in 2019, saw 24 per cent of the global fleet of ships and more than 17 per cent of worldwide cruises sail by, according to UNEP/MAP. The Arctic transitions restrict emissions in waters where polar shipping is small today but rising. The North-East Atlantic puts almost every major Atlantic transit under one regulatory regime.

The previous large-scale fuel rebuild — IMO 2020 — happened globally on one date. This one happens regionally over three years. A vessel that runs East-West routes outside the new ECAs is largely unaffected. A vessel that runs trans-Atlantic, Mediterranean, or Asia-Northern-Europe absorbs the cumulative change at each ECA transit. Most major trade lanes fall in the second category.

What the Mediterranean Showed in 12 Months

When the Mediterranean SOx ECA took effect on May 1, 2025, the industry knew the fuel mix would shift. Most analysts expected gradual adjustment. The data was sharper.

VPS tested approximately 1.61 million metric tonnes of marine fuel pre-ECA (November 2024 – April 2025) and 1.89 million metric tonnes post-ECA (May 2025 – October 2025) across the top 10 Mediterranean ports — about 90 percent of regional bunker volume. The fuel mix transformed inside six months:

Mediterranean Bunker Fuel Mix — Year One of ECA

Top 10 Mediterranean ports, VPS data, six months pre/post implementation

VPS reported VLSFO volume fell 23% in absolute tonnage. MGO usage rose 107%. ULSFO supply grew four-fold; biofuels five-fold. Total Mediterranean bunker tonnage rose ~20%.

The transition was not gradual. In six months, VLSFO ceded its dominant position. MGO doubled. ULSFO and biofuels — both at single-digit shares before the ECA — became material categories. Total bunker supply in the top 10 ports increased about 20%. The regulatory shift did not reduce regional demand; it reorganized it.

The single largest operational story was MGO. Marine gas oil — a distillate fuel already widely used as ECA-compliant fuel in the Baltic and North Sea — became the dominant compliant choice in the Mediterranean, ahead of ULSFO (which is purpose-blended at 0.10% sulfur). The reason is operational. Vessels with unpredictable Mediterranean schedules found it easier to keep MGO in dedicated tanks than to commit a tank to ULSFO, which is harder to source consistently and has its own quality concerns.

The quality concerns showed up in the data directly.

VPS recorded ULSFO off-specification rates rising from 2% pre-ECA to 20% post-ECA — a ten-fold increase. The main off-spec parameters were pour point, sulfur content, total sediment, CCAI, water content, and viscosity. The same supply chain quality gap that has historically affected VLSFO transitions appears to be repeating with ULSFO scale-up.

Year one showed the pattern. When an ECA goes live, the fuel mix moves immediately. MGO takes the dominant compliant share. ULSFO grows but with quality problems that compound at scale. Total bunker tonnage shifts, not contracts. The system around the new fuel catches up more slowly than the consumption.

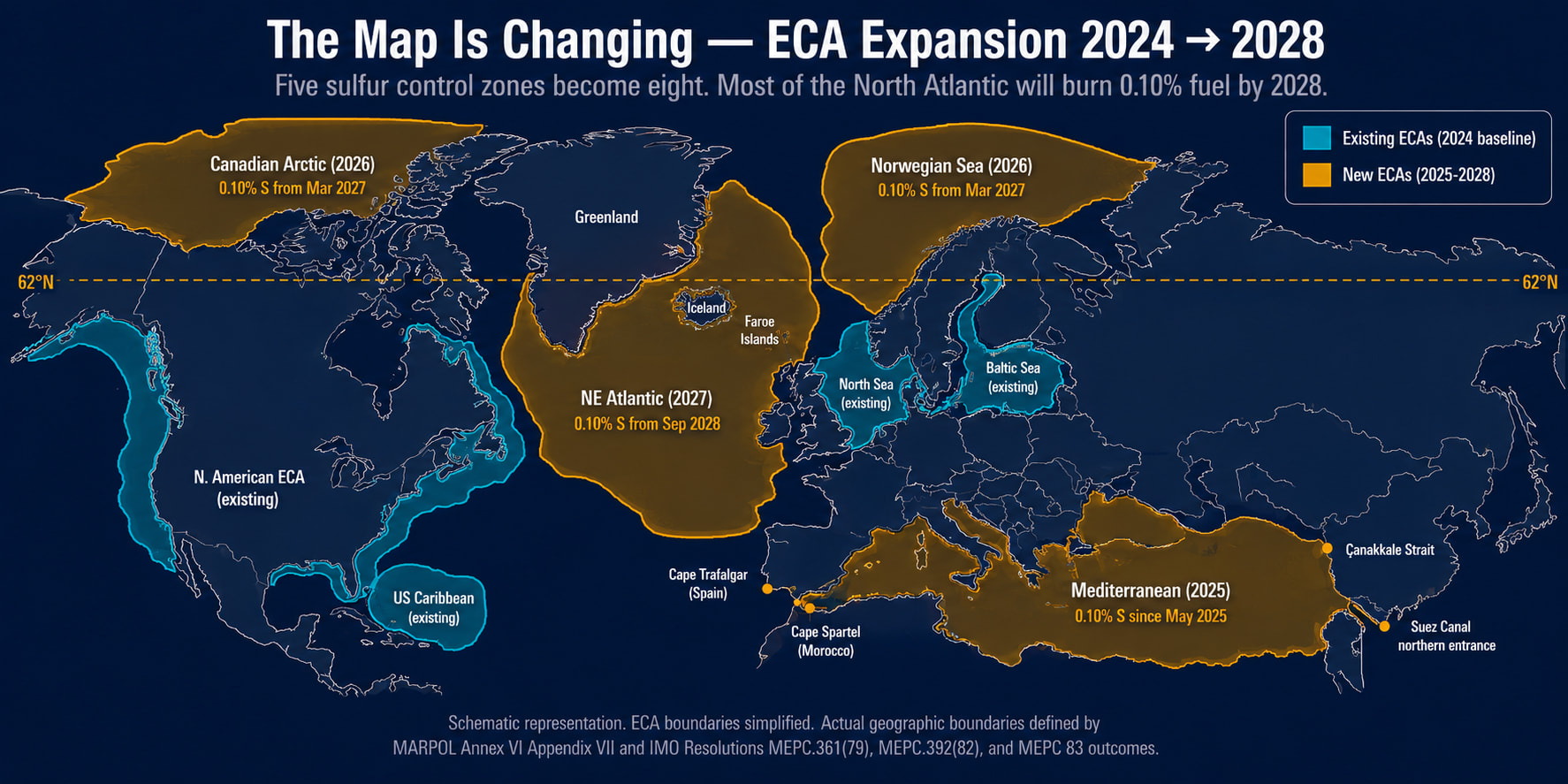

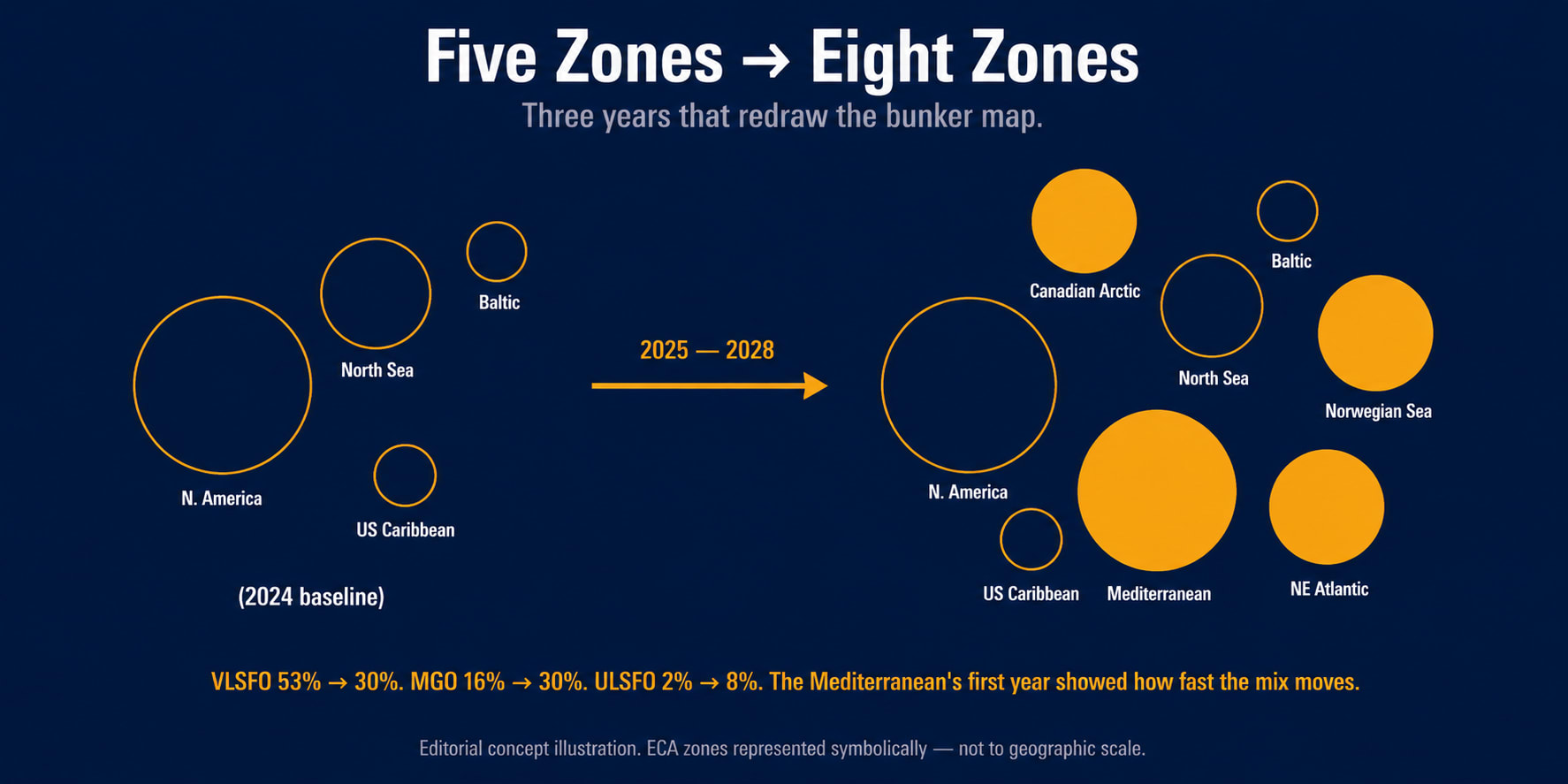

The Three New Zones, in Detail

ECA Expansion Timeline 2024 – 2028

Five zones become eight in three steps.

By 2028: eight zones, covering most North Atlantic, Mediterranean, and Arctic commercial traffic.

Each of the three new zones has its own geography and its own enforcement calendar. The differences matter for routing and fuel planning.

Mediterranean Sea (in force since May 1, 2025) covers all waters enclosed by the coasts of Europe, Africa, and Asia, bounded in the west by a line connecting Cape Trafalgar (Spain, 36°11'N, 6°02'W) and Cape Spartel (Morocco, 35°48'N, 5°55'W); in the northeast by the Çanakkale Strait (Dardanelles), defined as a line connecting Mehmetçik Burnu (40°03'N, 26°11'E) and Kumkale Burnu (40°01'N, 26°12'E); and in the southeast by the northern entrance to the Suez Canal, with a small specified exclusion zone at the canal mouth. SOx and particulate matter only. No NOx Tier III requirement.

Canadian Arctic ECA (entered force March 1, 2026; sulfur limit applies March 1, 2027) covers Canadian Arctic waters from the 137th meridian west in the Beaufort Sea east to the existing North American ECA boundary. SOx, PM, and NOx Tier III. NOx applies to ships with keels laid on or after January 1, 2025 — the older “single-date” principle.

Norwegian Sea ECA (entered force March 1, 2026; sulfur limit applies March 1, 2027) covers the Norwegian Exclusive Economic Zone north of 62°N latitude out to 200 nautical miles, reaching the Russian border, including Norwegian fjords and coastal waters. SOx, PM, and NOx Tier III. NOx applies under a “three-date” principle (see next section) — the first IMO ECA to use this framework.

North-East Atlantic Ocean ECA (expected to enter force September 1, 2027; sulfur limit applies September 1, 2028) covers the EEZs and territorial seas (out to 200 nm) of Greenland, Iceland, the Faroe Islands, Ireland, the United Kingdom, France, Spain, and Portugal. Excludes the EEZs around Madeira, the Azores, and the Canary Islands. According to VPS and industry classification societies, this will become the world's largest emission control area by area. NOx applies under the three-date principle: contract January 1, 2027, or (without contract) keel July 1, 2027, or delivery January 1, 2031.

Together these zones connect the existing Baltic / North Sea / North American ECAs into an almost continuous belt of 0.10% sulfur zones around the North Atlantic and Arctic. VPS estimates the combined ECAs will cover almost half of all Arctic coastal waters by 2028.

The Norwegian Loophole That Closed

The most consequential regulatory change embedded in the new zones is not the geography. It is the way Tier III NOx requirements get applied.

Until now, every IMO ECA with NOx Tier III applicability used a single-date principle: requirements applied based on the date the ship's keel was laid. Shipyards and owners learned to optimize around this. If a stricter requirement was approaching, an owner could place a contract early, ensure the keel was laid before the cutoff date, and lock in the older, less-stringent requirements for the life of the ship. The contract could be placed years before construction began. Delivery could happen years after the keel was laid. Only the keel mattered.

The Norwegian Sea ECA breaks that pattern. It uses what MARPOL Annex I has used for oil pollution rules — the “three-date” principle. For Tier III NOx requirements to NOT apply, a ship must clear three independent thresholds:

The Loophole That Closed

Norwegian Sea and NE Atlantic ECAs change how Tier III NOx requirements apply.

The Norwegian Sea ECA is the first IMO ECA to use the three-date principle. The NE Atlantic ECA will use the same framework. Going forward, regulatory avoidance through keel-date optimization is no longer available.

Under the older single-date rule (Canadian Arctic), Tier III applies if the keel is laid on or after January 1, 2025. The optimization path is clear: lay the keel before the cutoff and the ship is exempt for life.

Under the new three-date rule (Norwegian Sea), Tier III applies if ANY ONE of three windows triggers: contract on or after March 1, 2026, OR keel laid on or after September 1, 2026, OR delivered on or after March 1, 2030. To avoid Tier III, a ship must clear all three windows — contracted before March 2026, keel laid before September 2026, and delivered before March 2030. Miss any one and Tier III applies.

This is the first time IMO has closed the optimization loophole at the ECA level. The North-East Atlantic ECA will use the same framework. Going forward, the regulatory cost of new NOx zones jumps materially. The planning window that lets the regulation be sidestepped is gone.

For shipowners and shipyards, the practical implication is the same: Tier III NOx aftertreatment — typically Selective Catalytic Reduction (SCR) or Exhaust Gas Recirculation (EGR) — moves from “strongly preferred” to “structural” for any vessel that may trade in Norwegian Sea or North-East Atlantic waters after 2030.

Bunker Market Re-Segmentation

The Mediterranean data showed how an ECA reorganizes a regional bunker market in 12 months. The North-East Atlantic ECA, once it enters force, will repeat the process at much larger scale.

Pre-ECA Mediterranean bunker demand was about 21.5 million metric tonnes per year, dominated by VLSFO (Gibson Shipbrokers, 2024 baseline). Gibson projected in late 2024 that Mediterranean VLSFO demand could fall to roughly 6 million tonnes per year as the ECA matured — a 70%+ reduction in absolute terms. The first six months of post-ECA data was consistent with that trajectory, though the full transition will take longer than initially expected. ULSFO did not absorb the lost VLSFO volume; MGO did, with biofuels and HSFO (for scrubber-equipped vessels) filling the rest.

The North-East Atlantic ECA covers an area substantially larger than the Mediterranean, with bunker hubs at Algeciras, Las Palmas, Lisbon, Rotterdam, and Antwerp that handle major Atlantic flows. VPS expects the fuel mix shift to be at least as large as the Mediterranean's, probably larger, because the ECA will affect trans-Atlantic crude tanker, container, and bulker traffic that currently bunkers VLSFO before crossing.

This is friction redistribution, not friction reduction. ECA expansion does not reduce total bunker demand — the Mediterranean's first six months proved this, with total tonnage actually rising 20%. The friction was redistributed: VLSFO down, MGO up, ULSFO and biofuels expanded from small bases, HSFO held steady (with scrubber-equipped vessels absorbing the latter).

The operational consequences extend beyond bunker procurement. Refineries that supply the North Atlantic basin will need to rebalance away from VLSFO and toward distillate streams (MGO) and ULSFO blending. Bunker barge fleets in major hubs will need segregated tank capacity for ULSFO and MGO that they did not previously maintain. Scrubber-equipped vessels — about 30% of the global fleet — gain a structural moat that compounds across multi-ECA routes. A vessel running an Asia-to-Northern-Europe round trip will transit Mediterranean ECA, North-East Atlantic ECA, and possibly Norwegian Sea ECA depending on routing. The cumulative bunker cost difference between scrubber and non-scrubber vessels on such a voyage rises materially after 2028.

Routing and Voyage Planning Effects

For voyage planners, the new ECA map has three practical consequences.

First, bunker stops become routing decisions. Picking where to take on fuel before entering a long ECA transit matters more than it did before. A vessel crossing the Mediterranean from Suez to Gibraltar under the new ECA needs enough 0.10% sulfur fuel for roughly 1,900 nautical miles, plus a margin. Picking Singapore, Fujairah, or Port Said for the pre-ECA bunker affects both cost and timing.

Second, scrubber economics become route-specific. A scrubber vessel's economics depend on how much of its annual mileage is in HSFO-eligible waters. The cumulative ECA expansion shifts the balance. By 2028, a vessel running between Northern Europe, the Mediterranean, and North America will be in ECA waters for a much larger share of its time. The scrubber's economic case strengthens on those routes specifically.

Third, charter party language needs updating. Bunker quality clauses written for a world of mainly VLSFO need to account for MGO, ULSFO, and biofuel compliance, plus the off-specification rates that have appeared with the Mediterranean transition. Contracts that allocate fuel costs and quality risk between owner and charterer are getting rewritten as the new zones come into effect.

The map is still being drawn. The North-East Atlantic ECA could expand. The Mediterranean ECA could add NOx requirements at a future MEPC session. New zones — the Red Sea, the South Pacific — are under early discussion. The direction is clear: regional 0.10% sulfur zones are expanding, not contracting.

What This Means for 2028 and After

By the second half of 2028, the cumulative ECA expansion produces several structural changes to the global bunker market.

VLSFO becomes a non-ECA fuel. Its dominant share will be on Asia, Indian Ocean, South Atlantic, and Pacific routes that do not transit multiple ECAs. North Atlantic VLSFO demand will be materially reduced.

MGO becomes the default compliant fuel. The Mediterranean data showed MGO winning the share-of-compliance contest over ULSFO. The North-East Atlantic transition is likely to reinforce that pattern. Refineries will continue rebalancing toward distillate.

Scrubber-equipped HSFO operators gain a structural moat on multi-ECA routes. Their fuel cost advantage compounds over each ECA transit. By 2028, a vessel running an Asia-Northern Europe-Mediterranean round trip will spend a substantial share of its voyage in ECA waters. The non-scrubber vessel pays the compliance premium on every nautical mile. The scrubber vessel does not.

Tier III becomes universal for new ships trading the North Atlantic. Newbuild specifications written from 2027 onward will assume Tier III as baseline for any ship that may operate north of 62°N or in North-East Atlantic waters.

Refinery investment shifts. Refiners that supply Atlantic bunker markets will need to invest in distillate capacity and ULSFO blending. Refiners that supply Asian markets will be less affected.

The shipping industry has now had five years to absorb IMO 2020's global 0.50% sulfur cap. The next five years require absorbing a regional rebuild of that cap to 0.10% across most of the North Atlantic basin. The shape of that adjustment is already visible in the Mediterranean's first-year data.

Closing

Quiet Retreat (May 21) noted alternative fuels stalling at infrastructure. Two Clocks (May 23) noted dry bulk and tanker indices diverging. OCCS (May 24) noted carbon capture proving while infrastructure lags. The Houston Pattern (May 25) noted bunker quality gaps surviving across regulatory transitions.

The ECA expansion is the regulatory version of the same story. The rules work. The infrastructure to comply with them moves slower than the rules do. The Mediterranean's first year showed the fuel mix can shift sharply when the zone goes live. It also showed the quality, supply, and contractual systems around the new fuels catch up more slowly than the consumption — ULSFO off-spec rates rising tenfold from the moment the zone went live.

By 2028, eight zones. By 2030, possibly more. The molecule changes, the geography changes, the contracts catch up partway. The freight indices have not yet priced the cumulative premium. They will. The next bunker order placed for a 2028 voyage already needs to assume the new map.

The map is changing. The bunker market is rebuilding around it.